The idea of a robo-advisor conjures up thoughts of sci-fi movies featuring the likes of Arnold Schwarzenegger injecting you with some kind of financial DNA to make your investment decisions soar to levels beyond this world. Well, it’s not science fiction, but it isn’t nearly as ominous as Arnold was in the Terminator. Robo-advisors are digital platforms that provide automated, algorithm-driven financial planning services with little to no human supervision. So how does it work? The typical robo-advisor is accessed via your computer or smart phone, and will collect information about your current financial situation and future goals, and then uses that information to put a multitude of investing and asset plans together for you. Why use one? First and foremost is cost. These services build and manage an investment portfolio for you for a fraction of what the typical financial advisor might charge, allowing you to be hands-off with your investments.

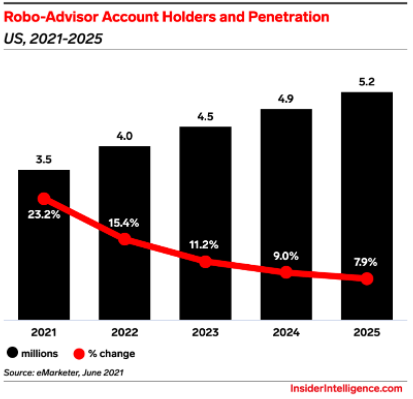

The number of robo-advisor services has swelled in recent years, as has the range of services. This year in the US, 3.5 million adult investors will use a robo-advisor to handle their portfolio. That’s up by 23.2% over 2020, which saw record growth of 37.4%. According to eMarketer, “The growth rate in the US will stay in the double digits for another two years, putting usage on pace to surpass 5 million adults by 2025.” Not too shabby.

So how exactly do robo-advisors do their thing? Well, most use some type of passive investment strategy that has at its core modern portfolio theory or some variant of it. MPT was developed by Harry Markowitz, an economist in the 1950’s, whose theory postulated that diversification was key to lowering the overall risk of a portfolio while maintaining the same rates of return. Portfolios would be rebalanced as the market moved one way or the other. Before robo-advisors it was costly and time consuming to constantly rebalance a portfolio, leaving it as something only professional investors could do. However, with robo-advisors this is both automatic and has virtually no-cost. Like a lot of fintech, robo-advisors are attempting to cut out the middle man and hence reduce costs to the user. The reduction in fees can be substantial. Most robo-advisors charge an annual flat fee of 0.2% to 0.5% of a client’s total account balance. That compares with the typical rate of 1% to 2% charged by a human financial planner.

Unlike a personal financial advisor, robo-advisors are available to access at any time on your time schedule. No appointments are necessary, just login to your computer or smart phone and start investing. In addition to notably lower fees, robo-advisors will work with individual accounts of all asset sizes, some starting with as little as $5. Alternatively, most wealth managers do not normally take on clients with less than $100,000 in investable assets, preferring high net worth individuals who can handle their fee structure. For the model to be successful in the long run the robo-advisors need to take on more clients than their human counterparts to make up for the reduced fee structure. However, these companies have alternative ways of bringing in revenue as well. One such is in the way they manage cash and cash balances of their clients. Typically, the robo-adviser will not pay interest on cash balances to clients and will take any interest credit themselves. Again, a large number of clients is needed to make what is usually a small cash balance significant. In addition, like their counterparts in the brokerage world, robo-advisors have access to another revenue stream in the form of payment for order flow. This is how brokers like Robinhood and others can effectively operate without charging commissions on trades. Typically, robo-advisors will accumulate funds that have been added from deposits, interest, and dividends, and then bundle these together into large block orders executed at just one or two points in a day. This allows them to execute fewer trades and get favorable terms due to the large order sizes. Lastly, partnerships are often formed with other financial companies, such as mortgage brokers, credit card issuers and insurance providers, all of which are attempting to market their financial services to the same client base.

As you might imagine, younger investors have really matriculated to the robo-advisor model for all of the reasons mentioned. According to Shelleen Shum, eMarketer senior forecasting director at Insider Intelligence, “Robo-advisors, well adapted to operating digitally, were able to cater to previously underserved customers like younger investors who are in the early stages of wealth accumulation.” So if you are so inclined to utilize one of these robo services, here are a few you might want to take a look at:

Vanguard Personal Advisor Services

- AUM: $206.6 billion

- Individual clients: 1.1 million

Vanguard has the obvious heavy hitter name recognition and ranks as the largest robo-advisor by assets under management. There are two advisory services that have a $3,000 and $50,000 account minimum balance, respectively.

Betterment

- AUM: $26.8 billion

- Individual clients: 615,000

Betterment and its AI software were one of the first robo-advisors on the scene, dating back almost a decade. Low fees and the ability to consult with a human financial planner are a big draw.

Acorns

- AUM: $4.7 billion

- Individual clients: 4.4 million

Acorns is kind of cool and caters to beginning investors. They began as a spare change app and are planning to go public this year at a reported valuation of $2.2 billion. The basic plan enables users to invest spare change and schedule recurring deposits into a portfolio of exchange-traded funds. Pretty cool.

Automated services like these have come a long way in recent years, making financial planning and wealth management available to everyone, regardless of net worth. If you are looking for a simple, straight forward way to get in the game, robo-advisors are a good option. However, given their nascence, they are probably still insufficient for those who need more sophisticated services, like tax management, estate planning and trust administration.