Don’t worry if you didn’t read Michael Lewis’s book, The Big Short, or even if you missed the cinematic version, you will get a chance to experience it again in another form. As I’ve I said many time before, history repeats itself, and you are doomed if you don’t know history. While on the subject, let’s take a brief stroll down memory lane and look at what most consider to be the genesis of what is known today as a collateralized debt obligation (CDO).

The genius of one Michael Milken, of the former Drexel Burnham Lambert investment firm, capitalized on the merger mania that was taking place circa 1987. Businesses were buying other businesses, so called raiders were making hostile offers to acquire companies or board seats. Money had to come from somewhere to pay for these takeovers. It came in the form of bonds, which eventually turned into junk.

Milken assembled portfolios of junk bonds issued by different companies and birth was given to the CDO. Securities firms subsequently launched CDOs for a number of other assets with predictable income streams, such as automobile loans, student loans, credit card receivables.

Before we throw out the old CDO and bring in the new, let’s do a basic primer on what this financial instrument is. The diagram above is a simplified graphic. The issuer of CDOs pools together cash flow-generating assets (like the bonds pictured above) and repackages this asset pool into discrete tranches (debt instruments that are split up by risk) that can be sold to investors. A collateralized debt obligation is named for the pooled assets, such as mortgages, bonds and other loans, which are essentially debt obligations that serve as collateral for the CDO.

Professional investors and those with private wealth are in aggregate lemmings who chase yield. Guess what, they are now chasing CDOs again. This time around it isn’t mortgages, but corporate debt itself. Wall Street argues that it is different this time around, since the collateral is not consumer debt in the form of sub-prime mortgages, but is that of corporate America.

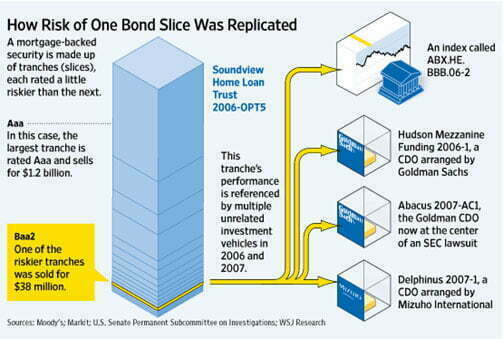

To add another layer of interest to the conversation, is that once again there is a synthetic, which acts in concert with the underlying CDO, which is the potential powder keg, because multiple investors can invest in the same synthetic CDOs. “It’s almost beyond belief that the very same people that claimed to be expert risk managers, who almost blew up the world in 2008, are back with the very same products,” said Dennis Kelleher, chief executive of advocacy group Better Markets. The graphic below may help illustrate the synthetic CDO.

The crux of the problem is that the bottom tranche was not just sold as Baa2 risk securities, but was combined with those on the right, that investors in general had no idea what they were. Such is a synthetic.

So where are we size wise in relation to the Great Recession of 2008? The current synthetic CDO market is much smaller than it was in 2008, however it appears to be growing. Again, the reason is yield. Investor’s willing to take the first losses on the underlying credit derivatives can receive yields of about 10 percent, traders say.

Trust me that catches eyes. Here’s the thing. Hedge funds, rather than banks, have become the big buyers, accounting for more than 70 percent of volume in the market. Banks are responsible for 10 percent of volumes, down from more than 50 percent five years ago, according to JPMorgan. As with risk arbitrageurs in the 80’s, the herd of hedge funds will be slimmed down as well if this CDO market goes south again. What comes around goes around.