Those that prey on the seniors in our society are using technology to allow them to access just about every faction of one’s life. This takes a special kind of hubris to commit fraud to those of the greatest generation and others. Now the U.S. government is getting into the act. Attorney General William Barr announced on Thursday that the Justice Department would be executing an “all-out attack” on fraud against seniors. Tech crimes are particularly despicable, and are being used to target American seniors around the world. Hackers from Eastern Europe, China, India, Russia and elsewhere, have no regard for the elderly in America. According to Barr, “The focus during this year’s probe was tech-support scams – where the criminal pretends to work for a company like Apple and tells the victim, for example, that his or her device has a virus. The criminal says it can be fixed for a fee and access to the device.” While the seniors on average may be easier targets of tech fraud, the general public is also being attacked. Justice Department statistics suggest that this year’s sweep includes charges against more than 260 defendants who allegedly defrauded more than 2 million people of more than $775 million.

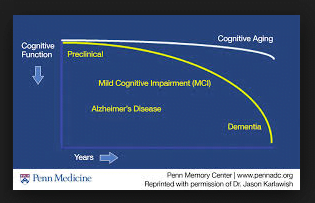

A white paper produced by the Securities and Exchange Commission in the summer of 2018 discusses elder financial abuse and the steps regulators are taking to combat it. The paper makes use of empirical evidence from Penn Medicine and the University of Pennsylvania, which denotes increased senior cognitive impairment as a key component of rising fraud. The Penn Medicine study goes on to say that cognitive decline is a key factor, whether brought on by disease or other changes in the aging brain even without the presence of disease. When cognitive decline begins, financial impairment is often one of the earliest signs for patients, families, and doctors. Physical decline and dependency are also risk factors for elder financial exploitation.

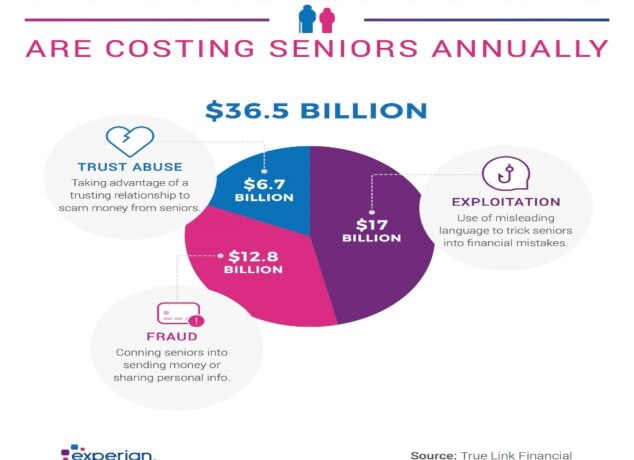

This cognitive decline plays out in the statistics as well. The Federal Trade Commission (FTC) states that, “Amounts reported stolen tended to vary by age: When those ages 70 and over lost money, the median value was $751, compared with a median of $400 for people in their 20s. The median was even higher for those at least 80 years old – at a whopping $1,700.”

According to the National Council on Aging (NCOA), there are three major trending scams that are currently targeting senior citizens:

- Fraudulent phone scams regarding Social Security

- Contact from “fake” grandchildren wanting money

- Phony post-natural disaster schemes to obtain money

So what can be done to help? The obvious is that any senior that thinks they are possibly the victim of a scam, to pass the word around. The FTC offers free materials you can download or order and share in your community to protect older adults from scams. The SEC has also taken a big step to prevent senior fraud by enacting tougher regulation in February of 2018. Essentially, this would allow designated financial firms to place a temporary hold on disbursements from the accounts of certain clients when financial exploitation is suspected. If you have family or friends that are seniors, pass this information along and don’t be afraid to discuss these important financial matters with them.