Just when you thought it was safe to go outside again without a mask and have life return to a sense of normalcy, along comes China again with draconian Covid lockdowns that are beginning to have a trickle-down effect on U.S. markets.

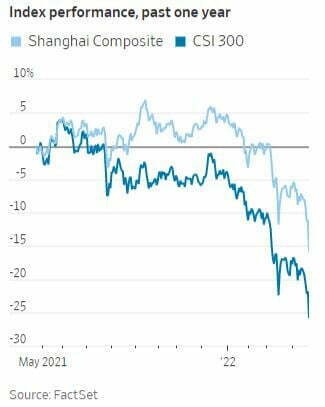

Chinese stocks suffered their worst selloff in more than two years and the yuan hit its lowest level since late 2020, as investors worried that strict policies to combat Covid would add to the pressures weighing on China’s economic growth and corporate profits. And it appears that the worrying was well founded. According to economists at the International Monetary Fund, China’s growth forecast is being cut to 4.4%, causing a mass exodus of foreign investment from both the Chinese debt and equity markets.

On Monday, the Shanghai Composite and CSI 300 indexes fell 5.1% and 4.9% respectively, marking the largest single-day percentage declines for both benchmarks since February 2020.

So you beg to ask the question, what do I care about what happens in China and to their economy. The average American I’m sure believes they deserve whatever deleterious financial events happen to them. Not so fast there my friend. There’s something called globalization and the give and take between markets of all kinds worldwide.

The Chinese flu with likely origins in Wuhan has reared its ugly head again in Shanghai and possibly mainland China as well. “The scourge of Covid continues, with China unwavering in its zero tolerance policy,” said Susannah Streeter, senior investment and markets analyst at Hargreaves Lansdown. These unforeseen Covid related lockdowns in China have led economists to redraw the map and bring a myriad of financial grief into play.

We went from what was thought to be transient supply slowdowns to supply issues lasting perhaps a year or so, on to what we have happening now. Currently, there is concern that prolonged lockdowns will hit employment and lead to a sharp slowdown in growth as well as sparking fresh shipping logjams and supply chain issues.

China is the world’s second largest economy and is going to influence everything from commodities to financial markets. Speaking of commodities, oil and mining companies are down as a result of the Chinese news.

Any type of lockdown will cause a classic demand shift economic situation where you will see prices falling on commodities as the demand for them subsides.

This is creating somewhat of an “imperfect financial storm,” so to speak. You have the aforementioned Covid-related disruption to supply chains, shortages and rising prices linked to the war in Ukraine, and of speculation the Fed and other central banks will hike interest rates faster than expected in an effort to keep a lid on inflation.

None of this was in the crystal ball at the beginning of 2022. According to Russ Mould, investment director at AJ Bell, “The prospect of further restrictions in China could lead to a poisonous mix of further inflationary pressure, as supply chains in the so-called ‘factory of the world’ get disrupted and weaker economic growth.”

Remember that markets always dislike uncertainty, which will bring volatility as it tries to determine direction in the face of these aggregate events.

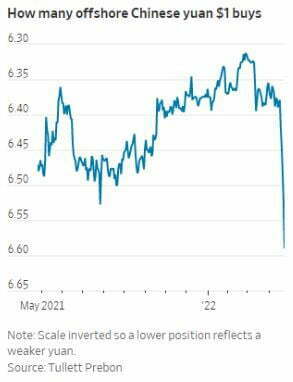

China was already on shaky ground before the notion of lockdowns arrived and was already showing signs of slowing down thanks to a property crisis and increased regulation. The growth fears come amid expectations of rapid interest rate hikes from the U.S. Federal Reserve, which could further prompt capital outflows from China and weigh on the yuan.

All of this is occurring during a back drop of China wanting to feature itself as a potential reserve currency of the world one day, replacing the U.S. dollar. The current market environment is exacerbating such attempts. The bond market is at the epicenter and one must remember that trading in another countries debt requires converting currencies.

As such, with U.S. Treasury yields rising, the relative appetite for Chinese debt has declined, and this liquidation has caused the yuan to plummet. The pain for China hasn’t just been in bonds and the yuan. Overseas investors offloaded 45 billion yuan ($7 billion) of stocks in March, the largest outflow in nearly two years.

Be careful if you are the owner of Chinese companies that trade in America. These securities are known as ADR’s, or American Depository Receipts, and allow foreign firms to trade on U.S. stock exchanges.

The sell-off in Chinese stocks has hit the Chinese ADR’s as well. In addition to the circumstances mentioned, regulatory risks in the U.S. have played a part in the latest downturn for Chinese stocks. The SEC revealed a Provisional List of new Chinese companies subject to delisting under the Holding Foreign Companies Accountable Act as it continues to crack down on foreign firms that refuse to open their books to regulators.

According to Morningstar senior equity analyst Ivan Su, “The SEC identifies what companies are subject to delisting as early as the firm files its annual report and on a rolling basis, therefore, we expect more Chinese ADRs to be included in the Provisional List over the next few weeks.”

Spokespersons for the China Securities Regulatory Commission as well as the State Administration of Foreign Exchange are assuring investors that the Chinese economy is resilient and that investors should have a long-term time horizon in yuan-denominated assets. The Chinese are optimistic that this environment will only be of a short duration, but you have to wonder whether this is just financial propaganda.