Bonds have been battered ever since we realized inflation wasn’t transitory, at least everyone but Janet Yellen, and since the Fed made it their mission to tame such inflation by raising interest rates.

Yes, it’s been ugly for bonds.

What was once a safe haven in times of turmoil and market volatility, has been anything but for bond investors this year. ETFs and other funds that track the bond market are off some 16% this year, while longer-term U.S. Treasurys have given back 34% compared to a 21% drop in the S&P 500.

Bond prices and yield move in opposite directions. As one would expect this has caused a mass exodus from the fixed-income markets.

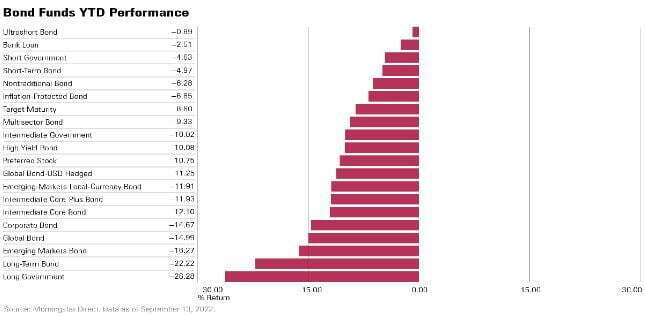

The following chart depicts the negative returns.

I think one of the most important things to remember is that holding a bond to maturity will almost always garner your entire principle back plus the stated interest or yield to maturity.

Certainly, U.S. Treasurys, municipal bonds, and investment-grade corporates fit this scenario. Fixed income has been the red-headed stepchild since the last recession through the currently ending decade bull market.

Why would anyone invest in bonds with a real return of close to zero when the stock market has returned on average almost double digits during the same period? Well, you wouldn’t, but the economic landscape is changing. As the bull market in equities turns into a bear market, spreads between the stock and bond market are narrowing.

Take a look at the municipal bond market for instance.

According to Jason Ware, head of municipal trading at InspereX, a bond underwriter, and distributor:

“Some bonds issued by state and local governments now yield about 4%, well above the level a year ago, and depending on the type of bond and where an investor lives—that could mean a tax-equivalent yield as high as 8% for those in top tax brackets.”

If we look at the numbers thus far this year a compelling case can be made for bonds. According to Fidelity Research, as of October 28, 2022, shorter-term Treasurys are yielding more than 4%, investment-grade corporate bonds around 6%, and high-yield corporate bonds close to 9%. These yields compare favorably with a total return of the S&P so far this year of −17%.

As bond yields approach that of historic returns in the equities market the pendulum is set to swing in the direction of bonds. Also keep in mind that among other things, your age and risk tolerance comes into play. If you are a recent high school or college grad, for instance, you can have a much longer time horizon and won’t be affected as much by volatility, as you have decades to weather the ups and downs.

Bond prices and yields are driven by market factors and change each day.

However, as mentioned, if you hold a bond to its maturity you will receive your principal plus the coupon rate, or the interest rate at that time. This has been a long time coming.

As Managing Director of Asset Allocation Research Lisa Emsbo-Mattingly puts it, “The Fed had been financially repressing savers, especially retirees. Now, though, rising rates mean that retirees and savers may once again be able to earn attractive returns without taking much risk.” As the following chart shows, bond yields have blown past that of dividends.

With the CPI down a modicum in November to 7.7%, we may be inching closer to the Fed’s target inflation rate of around 2.5%.

So what does this mean?

Perhaps the window of opportunity to lock in these competitive bond yields may be short-lived. If the central bank tightening does push the economy into further recession, the Fed will once again take its foot off the brake and will begin to bring rates down. As such, yields will drop and will be less compelling against the stock market going forward.

If you’re interested in adding bonds to your portfolio, you can choose from individual bonds, bond mutual funds, and exchange-traded funds as well as other bond-like fixed-income products such as CDs.

U.S. News suggests a hand full of bond funds that you should take a look at now.

- Pimco Income Fund (ticker: PONAX)

- Vanguard Short-Term Investment-Grade (VFSUX)

- PGIM High Yield Fund (PHYZX)

- BlackRock Strategic Income Opportunities Portfolio Institutional Shares (BSIIX)

- Invesco AMT-Free Municipal Fund (OPTAX)

Fixed-income securities are generally a part of a well-diversified portfolio but can be difficult for the non-financial investor to get a handle on.

It’s really best to work with someone who understands the nuances of the bond market and can match the proper securities to your risk-return agenda. The big takeaway is that as long as the Fed continues to raise interest rates, the window to buy any of the above-mentioned bonds is open.

Just like any market you probably won’t be able to time the moment when rates top, but you will certainly know that the top is near if we go into recession and the Fed begins to prime the pump by lowering rates again.

Many expect this scenario to play out in 2023, so act quickly if you want to secure some of these recent high bond yields.