The one thing that was fairly certain going into the markets this year was the fact that there would be volatility and lots of it.

So far, that would be correct. Daily swings in the equities markets of two and three percent have become the norm. Decades ago, that kind of percent move was made in a year and not in a day. Investors should buckle up because volatility is not going away. Inherently, volatility is measured by option pricing in the equities markets for bellwethers like the S&P 500 index. It can also be the standard deviation of a stock’s current price.

What one can’t predict, however, is the direction of the volatility, hence the difficulty in investing in the current markets.

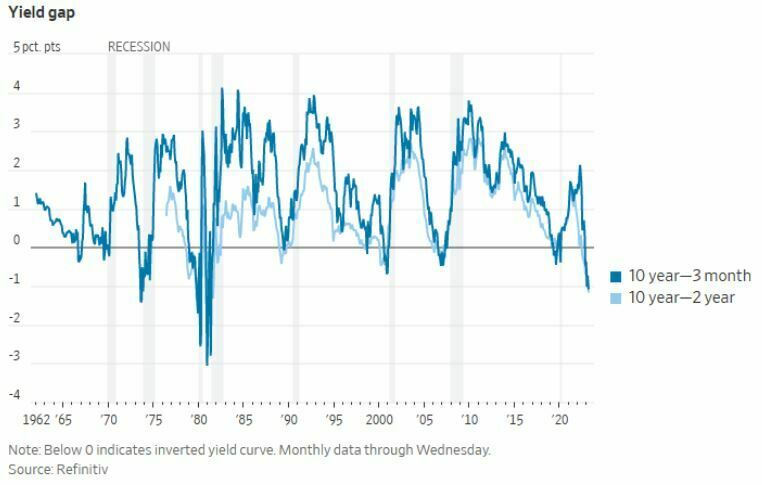

To make it all the more unpredictable, the markets themselves are diverging based on the particular asset group’s outlook on the economy. If you look at the treasury markets, you can determine that the odds of a recession are high. That wouldn’t be at all surprising, as this is the modus operandi of the Fed currently.

If you tighten monetary policy, you want an economic slowdown, albeit not to the point of a recession. The metric behind the recession reasoning lies in the yield curve and its inversion, which has historically been an indicator of recession for many economists.

The following chart shows the current inversion at its lowest point since 1981 for the 10-year Treasury against shorter-duration bonds.

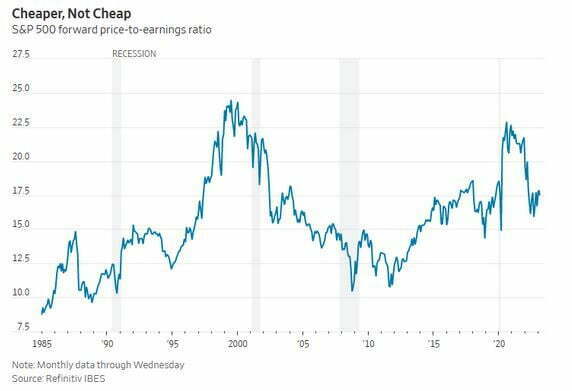

So what are risk-on assets telling us? The short-term up trend in a broader bear market tells us that they currently aren’t viewing the economy with the eyes of a recession looming. A recession does not generally bode well for stocks, as profits will decline, leading to lower shareholder value. The popular metric to view this is the forward earnings yield or profits as a percentage of the share price.

The chart below depicts that while stocks are relatively cheap, they are historically high compared to the lows made in the dot.com bubble.

If we look at equities compared to corporate bonds, stocks are still pricey in today’s dollars. High-yield bonds, or junk bonds, were introduced in the ’80s by Michael Milken and Drexel Burnham Lambert.

These deb securities are typically rated as average, C, or below by Moody’s or other rating agencies. The ICE Bank of America High Yield index, offers about 4 percentage points more yield than equivalent-maturity Treasurys, compared with an average since 1996 of more than 5 points. According to the Wall Street Journal, this spread rose above 10 percentage points in all three recessions since then as investors worried about defaults. Big losses for junk will be on the way if a recession hits.

Uncertainty in the markets, as expressed in volatility and non-correlated asset markets, makes it difficult to predict the future but screams for a diversified portfolio in the long term. Even adequate diversity wouldn’t save the masses from losses in 2022.

The U.S. stock market, measured by Standard & Poor’s 500 indexes, ended 2022 with a total return of -18.11%. A key measure of overseas stock performance, the MSCI EAFE Index, returned -14.45%. Based on the Barclays U.S. Aggregate Bond Index, the U.S. bond market was down 13.01% on a total return basis. In this rare environment, it was difficult for investors to protect their portfolios.

What should you expect in 2023, and should portfolio adjustments occur?

In uncertain times cash can be king. Just ask Warren Buffett, who is sitting on over $2 billion of cash as of his latest annual report.

Online savings and cash management accounts provide higher rates of return than a traditional bank savings or checking account.

Capital One, for example, is offering a 3.4% APR currently. Not too shabby. But before you start thinking about high-yield savings accounts, take a look at your debt and see what interest rates you’re paying. In all likelihood, it’s much higher than any rate you would receive from high-yield savings. For example, saving $1,000 in a high-yield savings account at 4% interest would earn about $41 in a year.

But that same year, a $1,000 balance on a credit card with a 20% interest rate would cost you roughly $170 (assuming you make only the minimum payments).

According to Jose Hernandez, a certified financial planner with Crossroads Planning, “I know it’s not as fun as building assets, but if you’re flooded with high-interest debt, it may make sense to at least get that more manageable, and then when you’re in a position where you have more cash flow you can start investing.”

The initial stage of asset repricing (declining investment values) occurred in 2022, tied to the inflation threat and the Fed’s aggressive interest rate hikes.

According to Eric Freedman, chief investment officer for U.S. Bank, “A second wave of repricing may create additional downward asset price pressure,” in the coming year.

As such, shorter duration Treasury’s are something to look at, according to Freedman. The current yield on the 2-year Treasury note is almost 5%, a much higher rate than was available a year ago.

The crystal ball is currently not crystal clear, so it’s important to think about your objectives and station in life.

Determine whether there are opportunities to rebalance your portfolio to more appropriately reflect your investment objectives, risk tolerance level, and the current market environment.