The commodity prices of gold, oil, and others have been rising of late as uncertainty looms on the economic horizon.

Historically in market conditions as these investors will take safe haven in government bonds that are ostensibly risk-free. Much has been said about the outlook of the dollar recently as the reserve currency of the world. BRICS nations and others have incentives to move away from the dollar, using their own currencies to transact business in oil and other goods.

The Fed’s quantitative tightening has made treasury bonds less attractive to hold as shorter-term liquid assets. If you’re not able to hold these bonds to maturity, you become exposed to systematic market risk.

Just ask SVB or Signature Bank.

So what’s left?

As traders know, there is a strong correlation between inflation and commodity prices. When inflation accelerates at a red-hot pace, so do the prices of commodities.

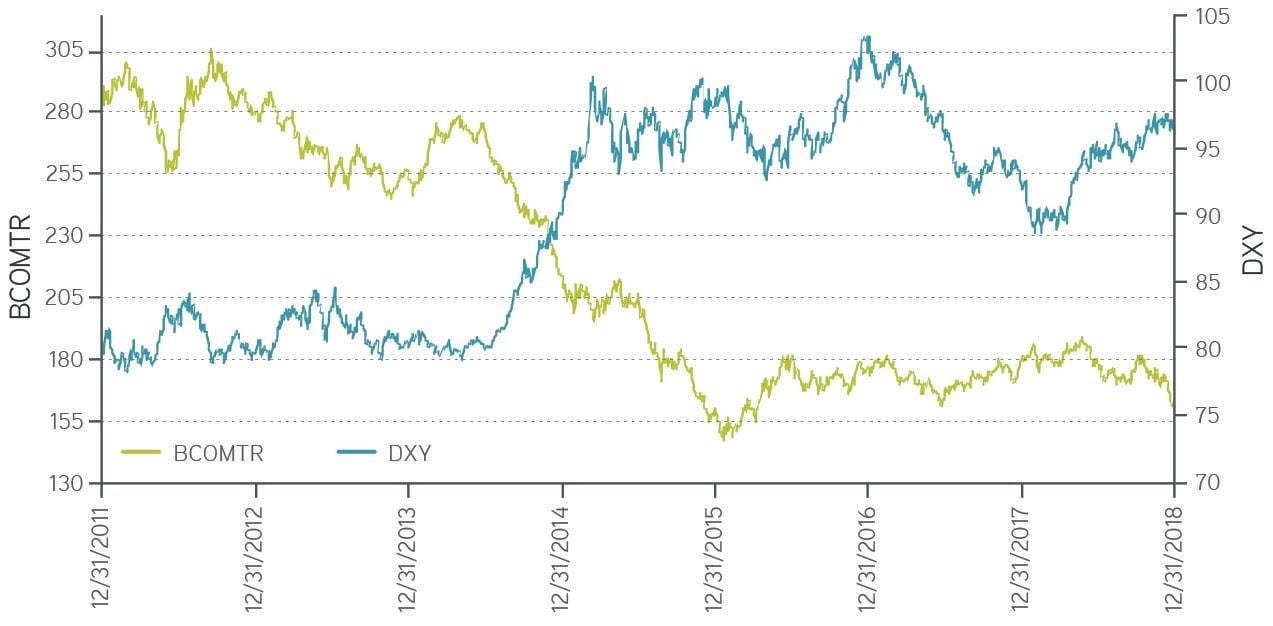

The dollar (USD) strength has traditionally been a headwind for commodities. Most major commodities worldwide are priced in USD, so buying commodities becomes more expensive in non-USD currencies when the currency strengthens.

As one strengthens, the other weakens.

The relationship can be seen graphically when comparing the dollar to a basket of commodities.

Let’s take a look at gold and its relationship to the current market conditions.

Gold prices last week came within striking distance of hitting all-time record highs reached in August 2020, while silver prices raced above $25 an ounce. Gold has moved from the $1,800 level at the beginning of March to above $2,000 an ounce this week, notching an impressive gain of over 12% in the past month alone.

According to Bloomberg Intelligence, spiking energy prices may have prompted central banks to tighten more than necessary, which could swing the other way in 2023, supporting gold.

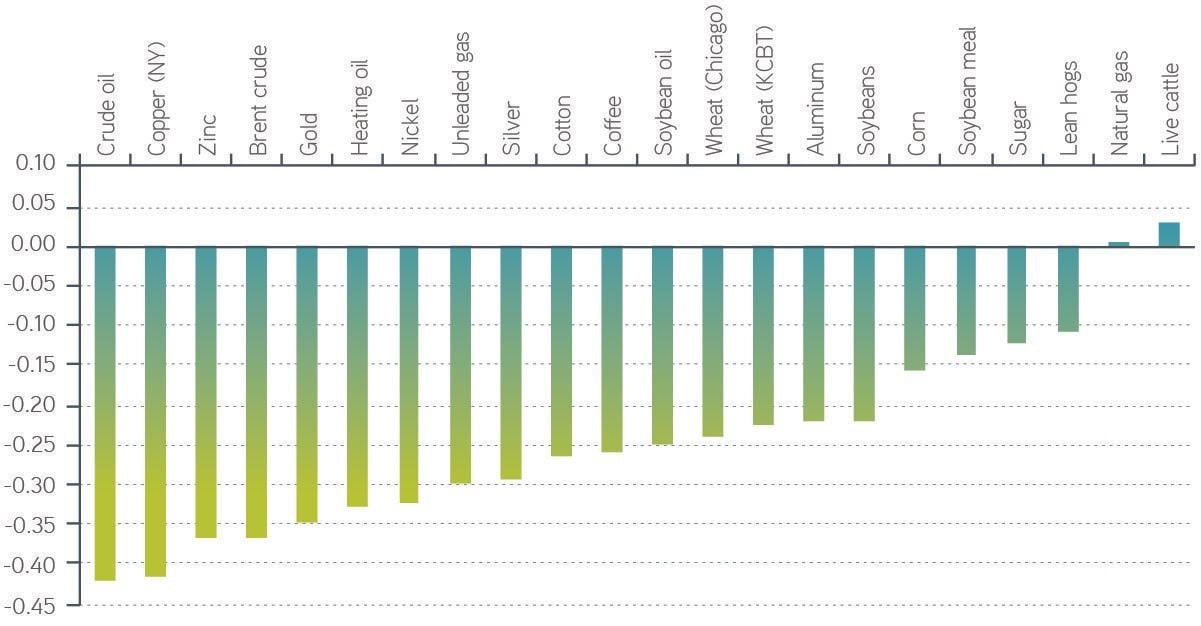

For almost all commodities, the chart below shows a negative correlation, meaning commodity prices tend to fall when the dollar strengthens.

This reinforces the idea of an inverse relationship between movements in commodity prices and the strength of the US dollar.

Goldman Sachs Commodities Research has been hyping an underinvested super cycle in commodities for several years. According to Goldman, from a fundamental perspective, the setup for most commodities this year is more bullish than it has been at any point since they first highlighted the super cycle in October 2020.

The one question that remains is can commodities top the returning act they’ve done in the last two years.

The Goldman Sachs Commodity Index (GSCI) was the best-performing asset class in 2022, posting some 23% returns.

This was on the heels of spectacular returns of 42% in 2021. Similar to other asset classes, commodity prices have peaks and valleys, but what is different is that, unlike financial markets, commodities perform an economic function of balancing supply and demand, so once high prices have rebalanced the market in the short term, the high prices are no longer needed, and prices come crashing back down as we witnessed late last year.

The two big wild cards that could make the commodities markets volatile this year are the war in Ukraine and the post-Covid Chinese economy.

Prices of agricultural commodities will continue to be influenced by events in the Black Sea region, specifically any extended agreements allowing Ukraine to export wheat.

The war will also indirectly impact other agricultural commodities due to high fertilizer prices resulting in shortages. Regarding China, much will depend on how quickly China opens up its economy in 2023. Depending on how much China’s property slump continues to curb construction activity, fiscal stimulus could represent an upside for steel and base metals.

It’s reported that China is firing up one new coal plant per week.

Most of China’s industrial production runs on coal power. Another likely winner as coal was the best-performing commodity in 2021-22 as Europe switched back to the commodity as a result of rocketing gas prices.

We’d be remiss if we didn’t mention the climate, not necessarily climate change, regarding commodity supply and demand in 2023.

Weather played a major role in commodities in 2022 and will probably do so again in 2023. Scorching heat waves hit wheat production in the northern hemisphere, and extreme weather will be detrimental to crop production in the first half of 2023.

As supply goes down, prices go up.

Summer temperatures will dictate the energy markets moving forward. Europe’s heatwave drove up demand last summer, causing gas and electricity prices to spike.

Whichever way you look at it, one thing is clear. Commodities are many analysts’ favorite trade right now, and that trend is set to continue throughout the rest of 2023.

The explosive cocktail of events that are currently unfolding now ultimately positions commodities as possibly one of the most lucrative and must-have asset classes in every portfolio.