Anyone who works with numbers or statistics knows that they can be powerful indicators, but they can also be misleading and make situations appear different than what they may be. Take the current market for stocks. The S&P 500, the bellwether indicator of overall market performance, is up 12% yearly.

Not too shabby.

That would imply about a 25% return for the annualized year. Those are pretty feel-good numbers. However, they may be misleading. If you remove the contribution of seven big technology companies in the index, the S&P would be negative for the year. That’s not a financial headline that you see every day. That potentially leaves the index vulnerable to a steep pullback if even one or two big companies misstep.

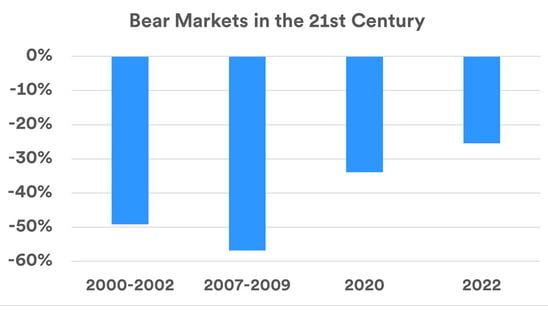

Four bear markets have occurred in the U.S. stock market in the 21st century. As you can see by the data in the following graph, the most recent bear market in 2022 was not as great as the other three.

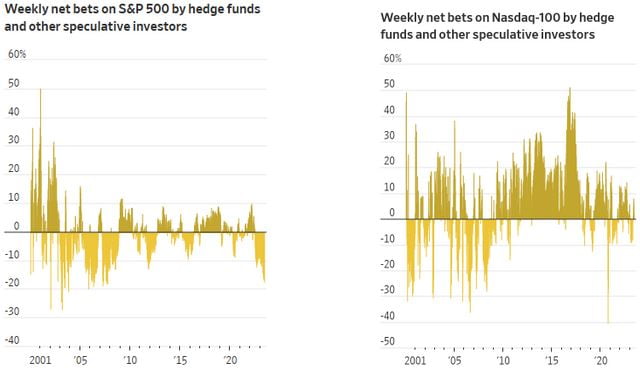

Suppose you look at the positions of hedge funds and other market speculators. In that case, you will note a bearish take on the broader market for the second half of 2023, as measured by data taken from the commitment of Traders report at the Commodity Futures Trading Commission. One can glean that large investors are cold on the S&P 500, while placing bullish bets in technology via the NASDAQ 100.

As the following two charts depict, open interest is currently higher in the NASDAQ 100 compared to lower readings in the S&P 500.

Bespoke data, which comprises and analyzes CFTC information, among other things, points out that shares of the ten largest companies in the S&P 500 climbed 8.9%, while the other 490 fell 4.3%. If you think you are currently getting diversification in the S&P 500, think again.

Tech stocks are back in a familiar position at the top of the stock market’s leaderboard after slumping last year, largely due to the growing interest and appetite for anything related to generative artificial intelligence technology.

According to U.S. Bank Wealth Management, the main takeaways from the current market environment are the following.

- U.S. stocks have recovered some ground lost since reaching bear market lows late last year.

- However, stocks seem to be “on pause,” unable to sustain enough momentum to recover all the ground given up in 2022.

- Expectations for a slower economy contribute to a challenging environment for stocks in 2023.

Ultimately no one knows what the future will hold, but several macroeconomic issues are holding court currently. Persistent inflation is at the top of the list. While supply chain issues and rising energy prices are mostly behind us, inflation is still present in the form of higher prices on basic necessities, as well as gains in employment and earnings growth among workers.

Inflation is ultimately the result of interest rate policy at the Federal Reserve. The Fed’s 2022 monetary policy shift was a key driver of the stock market’s bear market turn. The Fed hiked the short-term federal funds rate, from nearly 0% in early 2022 to almost 5.00% by March 2023, a significant attempt to slow inflation.

According to Eric Freedman, chief investment officer at U.S. Bank Wealth Management, “The question is how much further inflation must level out before the Fed is again willing to change course on interest rates.”

A third piece to the puzzle will be corporate earnings. Typically businesses have their fingers on the pulse of the economy and will let that be known through their financial statements as well as their forward looking vision. What we are seeing with recent financial reports is that businesses are tending to pass along higher prices to consumers, even if their cost of goods sold hasn’t risen as significantly. We’ll have to wait and see if this is a trend, and if consumers will oblige corporations and continue to come to the consumption table.

Now that the debt ceiling has been taken off the table by passing Congress and getting Biden’s signature, the once looming threat is no more. However, there are still potential worldview threats that remain imminent. The Russia-Ukraine war is currently a stalemate with its effects posing less immediate economic challenges for the U.S. and the world.

With that said, markets could certainly react to any major development that shifts the conflicts current course. The ever-present U.S.-China tensions have again flared up, causing the markets potential angst. The latest military tit-for-tat in the South China Sea is just another example of how fragile current relations are between the two military and economic superpowers.

On the economics front, it appears to be business as usual, but at times China’s priorities appear to be at odds with our economic partnership.

Any attempt by China to get involved in the Russia-Ukraine war by supporting the Russian military will bring certain volatility to the markets. In addition, the growing speculation that China will assume control of Taiwan in the coming years is likely also to unleash unknown chaos on the markets.

Buckle up!