Wouldn’t it be nice to have a crystal ball that would accurately predict where the stock market is headed next? I remember one of my finance professors once asked the class what section of the newspaper they would most like to have the day before if it was possible. Answers ranged from just about anything you could wager on, from sports to stocks.

He told us that if we could have just one day’s information ahead of time on the financial markets, the leveraged futures markets in particular, we would never have to work again.

While AI hasn’t yet quite figured that out for us, there are still a few modest economic indicators that have had an uncanny ability to accurately predict what happens next in the stock market.

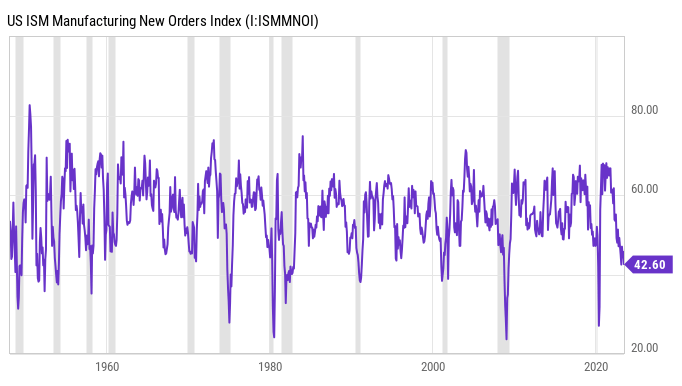

At the beginning of every month, market participants and the business press focus on the survey published by the Institute for Supply Management (ISM), the ISM Manufacturing New Orders Index. Currently, this economic indicator has been nothing short of flawless in predicting the directional movement in stocks over the past 70 years, and has a pretty clear message for where equities are headed next.

Let’s take a look at what exactly is the ISM Manufacturing Index and why it is so prescient in its financial forecasting.

The ISM manufacturing index, also known as the purchasing managers’ index, is a monthly indicator of U.S. economic activity based on a survey of purchasing managers at more than 300 manufacturing firms. It is considered to be a key indicator of the state of the U.S. economy.

Formally called the Manufacturing ISM Report on Business. The Manufacturing Index report outlines index movement for manufacturing, new orders, production, employment, inventory, prices, and backlogs. We are particularly interested in the new orders portion of the survey.

The ISM New Order Index shows the number of new orders from customers of manufacturing firms reported by survey respondents compared to the previous month. A reading over 50 shows orders have risen from the previous month while a reading below 50 shows a decline in orders. A reading of 50 would suggest no change from the previous month.

So far this year a handful of technology companies, mostly Big Tech related to AI, have had a phenomenal start to the year. However, the broader indexes as a whole have lagged, leaving investors wondering whether we are actually out of the woods of a bear market or not. As the above chart indicates, the manufacturing industry, a key driver of the U.S. economy, is still shrinking, and new order activity indicates more contraction is yet to come.

Things have been weak for a while.

The index for new orders has been below 50 for the past seven months. According to research from Ed Clissold, the Chief U.S. Strategist at independent research firm Ned Davis Research, the somewhat arbitrary line in the sand has been a reading below 43.5.

Out of the more than one dozen instances where the ISM Manufacturing New Orders Index has produced a reading below 43.5, only one proved to be a false-positive for a U.S. recession, and that was 70 years ago. Since then, any time the New Orders Index has dipped below 43.5, a recession has followed soon after. Multiple times in 2023, the ISM Manufacturing New Orders Index has fallen below 43.5.

If you’re still not convinced of the validity of the ISM Index, there are a couple of other macro indicators that will catch your eye.

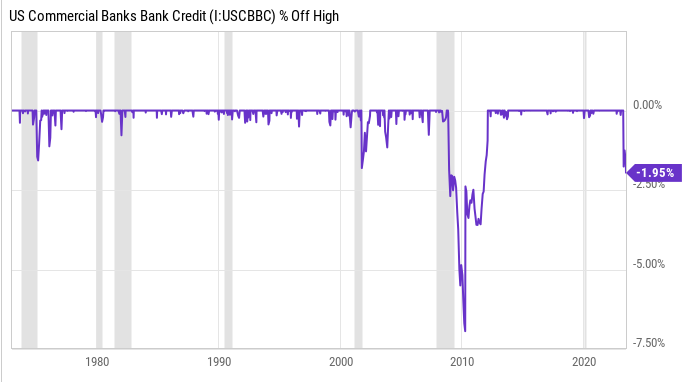

One of them has to do with commercial banks. Banking is very simple. People need money and banks have it to lend. When this type of lending is in jeopardy, as it currently is, there is demonstrable downside for the markets in general.

The failure of SVB Financial’s Silicon Valley Bank, followed by Signature Bank and First Republic Bank being seized by regulators, has banks very clearly tightening their lending standards. This does not bode well for overall economic activity. Since the early 1970s, there have been four instances where commercial bank credit declined by at least 1.5% from an all-time high.

Three of these periods coincided with the benchmark S&P 500 losing about half of its value. The fourth such instance has been ongoing over the past several months.

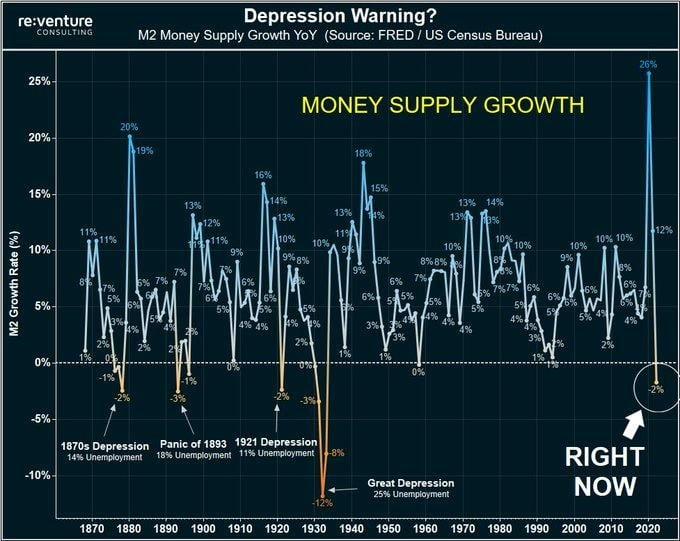

Money supply can also be a precursor for market volatility. The most liquid measure of money in circulation is M1, which includes physical coins, cash bills, and checking accounts, followed by M2, which encompasses all of M1 plus savings accounts, money market funds, and CD’s under $100,000.

Contraction in the money supply can ring alarm bells for the economy.

Money supply as measured by M2 has only contracted 4 times in the last 150 years, each time followed by a double-digit unemployment rate and a depression, according to Nick Gerli, CEO of Reventure Consulting.

It would seem, however, that with rates rising on demand deposits, savings accounts and other M1 and M2 components, consumers will begin to transfer money into these accounts for higher yield with essentially no risk.

The moral of the story is that if you are in the equities market for the long term, these shorter term bear moves will be but a blip on the stock chart.

While it’s true that we’re never going to know ahead of time when these downturns will begin, how long they’ll last, or where the bottom will be, we do know, from history, that the major indexes move higher over time.