It’s that time of year again to start thinking about paying Uncle Sam his share, and God knows he needs it this year with massive record federal deficits. He also has a newly minted mult-billion dollar IRS staff to make sure that you are on your toes, file on time, and don’t make any mistakes that might cause you to be audited. No stress at all. The market is up again thus far this year, albeit considerably less than 2022, but nonetheless one must plan on how to handle taxes on such gains.

With that said, there are ways to lower your tax burden, as long as you don’t procrastinate the time away, which is the number one cause of missed opportunities. First and foremost tax considerations should take a backseat to your investment fundamentals. If you are a long term holder of securities and that is your game plan, don’t sell just because of the tax implications. According to Roger Young, a certified financial planner and thought leadership director in the individual-investors division at T. Rowe Price, “Remember to focus first on investing fundamentals rather than taxes.” Also, beware of the water cooler scuttlebutt, as every person is different and has differing circumstances that affect their investments and taxes.

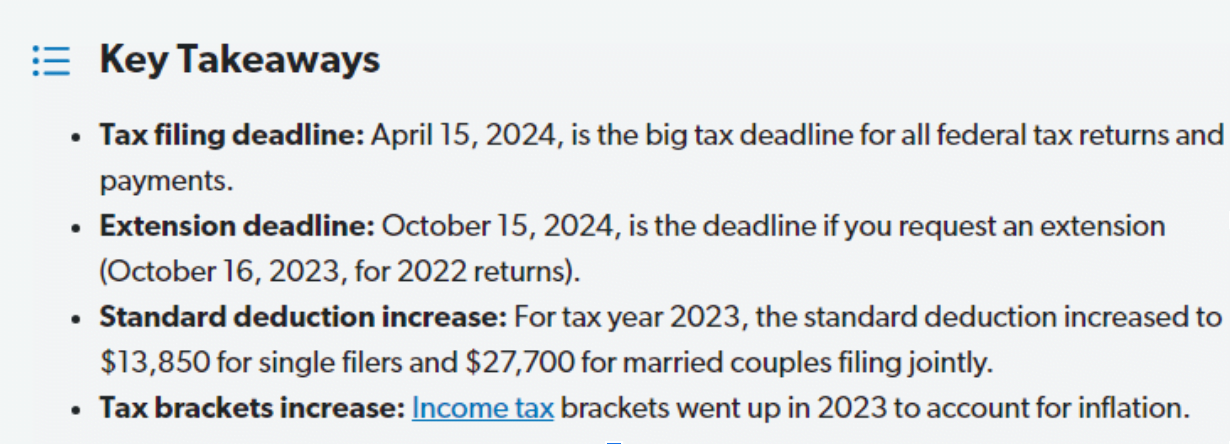

Take a look at some key takeaways for tax year 2023:

Also, before you begin, make sure to consider how any tax law changes may affect your taxes. The Consolidated Appropriations Act of 2023 is one example for this year. While the bill contains a variety of retirement provisions, some of the most important changes take effect in 2023. It is also important to remember that some tax opportunities in 2023 may go away by December 31, 2025, when the 2017 Tax Cuts and Jobs Act (TCJA) expires.

Evaluate Losing Securities

Even if you are a buy and hold investor, there are times and certain securities that you may want to give up and take a capital loss on. Not all companies are created equal as we know and some that are down for fundamental reasons may not come back. By selling a stock at a loss you can count this against any gains. This is known as tax-loss harvesting. Remember though, this advice doesn’t pertain to stocks held in tax favored accounts like IRA’s and 401K’s. According to Patrick Daly, tax partner, high-net-worth group co-leader, at Citrin Cooperman Advisors, “It may be especially important this year for many investors stung by the financial markets’ mood swings and higher interest rates.”

It’s possible that in 2023 you had losses that are larger than your gains. If this is the case you can do a couple of things. You could carry over the losses to the following year, or you could deduct up to $3,000 of capital losses against ordinary income like your salary. However, losses can’t be applied to real assets like your home or car.

Mutual Fund Distributions

Perhaps the only thing worse financially than losing money is actually having to pay taxes on top of the losses. This is a peculiar quirk with mutual funds, but is likely to transpire this tax season. You’re probably thinking to yourself, I don’t remember selling any mutual funds this year, so how in the world would I have to pay taxes. Especially since most of the funds that you are likely to own are down for the year.

Enter the not-so-transparent world of mutual funds. This one-two punch to investors happens as a result of fund managers having to sell holdings to raise cash to pay investors who are leaving the fund. This typically will trigger capital gains taxes for those who remain in the fund. According to Mark Wilson, a financial adviser with Mile Wealth Management who tracks large mutual fund distributions at CapGainsValet.com, “This is a salt-in-the-wound year. You owe taxes when you’ve lost money, and you have less invested going forward.”

Charitable Contributions

Making charitable contributions can decrease your tax bill, and could especially help those in higher tax brackets, since high‐income earners generally pay taxes at higher rates, they may enjoy a particularly large tax benefit from charitable contributions. For those that take the standardized deduction, there is a benefit in donating stock that has appreciated in value. This allows you to deduct the fair market value of the stock as a charitable donation, thus avoiding capital gains taxes, as long as you’ve held the stock for at least a year.

With uncertainty as to how charitable contributions will be taxed under next year’s rules, it is generally advised that you act on them this year. According to Lawrence Katzenstein, an attorney specializing in charitable planning with Thompson Coburn in St. Louis, “If you wait until Dec. 31st that may be too late. At least check with your broker to determine how quickly the firm can make a transfer.”

If you have a complex financial life, decreasing your tax liability requires a strategic plan. One change here could have unintended consequences someplace else, and could defeat your tax-savings strategy. Depending upon your level of financial sophistication and complexity of return, don’t hesitate to seek counsel from an accountant or tax attorney.