If you’re like the vast majority of American homeowners you locked yourself into a pretty good rate a few years ago before the Fed started its draconian tightening. That’s the good news. Lower rates mean lower interest payments and equity will build faster. The downside is that moving for moving’s sake isn’t really an option, because you don’t want to give up a 3 percent mortgage for one around 7 percent today. It can be disheartening if you need access to the equity that you have accumulated. Even with rates where they are you can still snag a loan that makes financial sense.

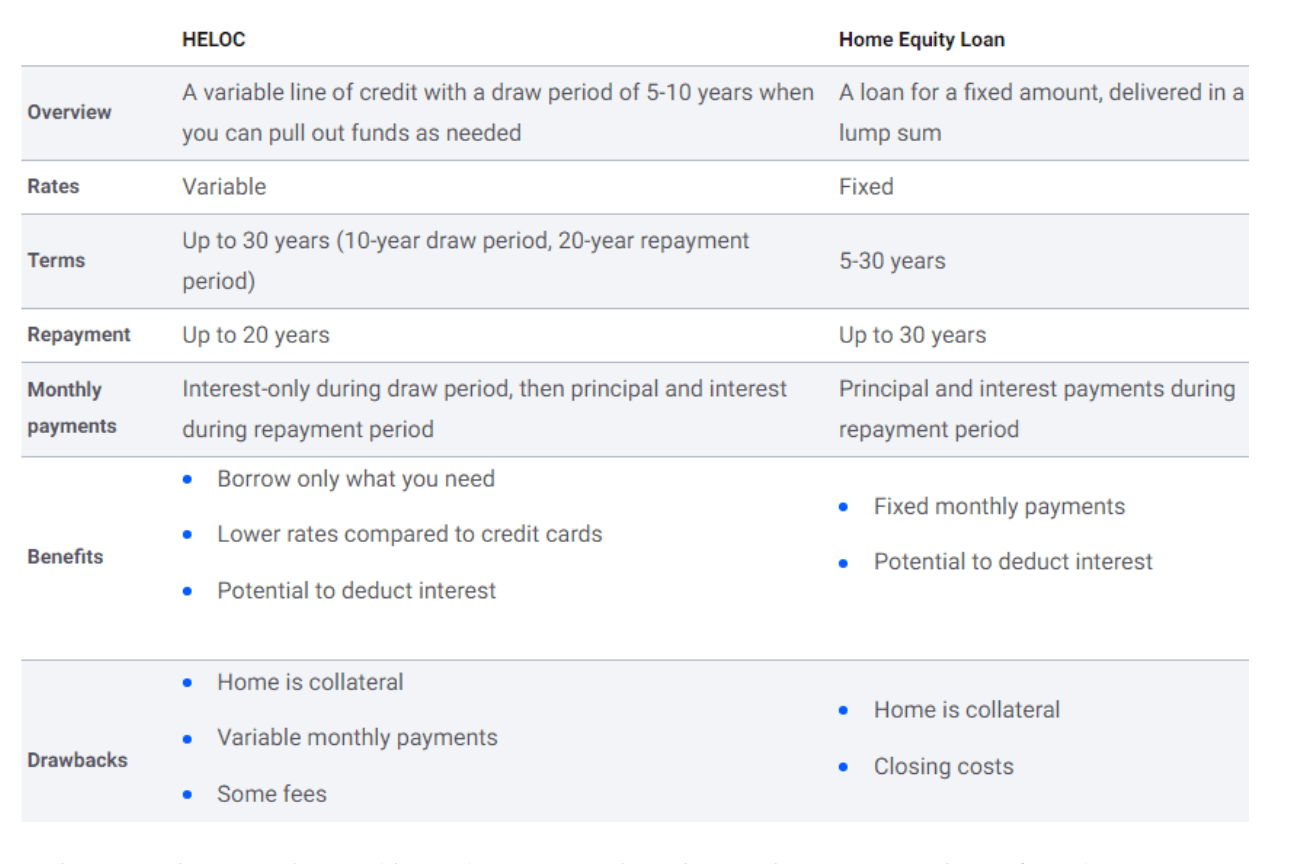

There are really two basic ways to get equity out of your house, one is the traditional home equity loan, and the other is a home equity line of credit or Heloc. Both are popular and depending upon what you are needing the money for, one might make more sense than the other. If you’re in the market for one of these two products you’re not alone. According to TD Bank, over half of homeowners surveyed in America are interested in one of these equity options. Here is a quick comparison between the two:

So what exactly is a Heloc and how do rates work with it? A home equity line of credit is a second mortgage that gives you access to cash based on the value of your home. You borrow against your equity, which is the home’s value minus the amount you owe on the primary mortgage. According to Bankrate, you can usually borrow up to 85% of your equity, though this varies by lender. The Heloc is similar to a credit card, in that you only have to draw down on it for what you need, and the interest rate charged is less than a credit card since it’s backed by the value of your home. Rates vary by lender, but are generally based upon the following:

- The amount of equity you have in your home

- Your credit score and history

- Your debt-to-income (DTI) ratio

- Your income history

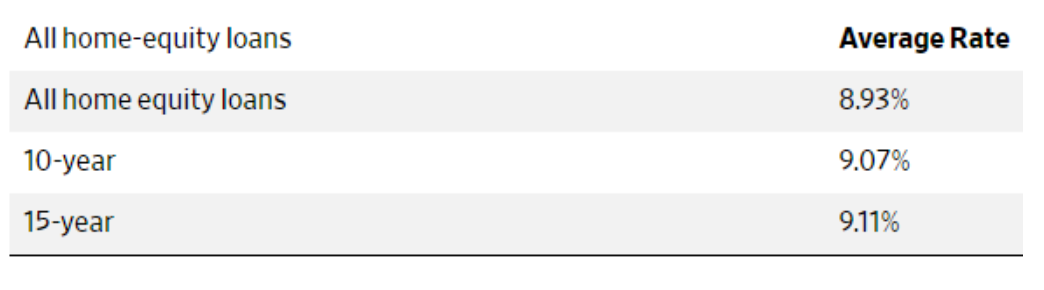

While still a solid value comparted to credit cards, rates for Helocs have risen as well. At the start of 2022, the average 10-year home-equity loan rate was 6.03%, and the average 15-year one was 6.09%. Here’s a look at where average home-equity loan rates stand as of December 2023:

Depending upon when you might need the funds from your loan, the question arises whether it makes sense to take out a loan now or wait for rates to potentially drop. According to the CME Group Fed Watch Tool, which uses futures pricing data to gauge market sentiment, it suggests most investors think the Fed will keep rates at current levels at least through the winter. However, there is a 50/50 chance of a rate decrease in the coming spring and summer, but whether it is enough to make a difference one can’t tell. As such, most economists see rates in the 8% to 10% range in the near term, with a slight drop in the spring and summer. Many think this is the high water mark for rates, so unless you’re in a hurry, rates on Helocs and home equity loans are likely to fall in the coming year.

Remember that unlike a credit card, your home equity loan or Heloc is secured by your home, so there is always a risk of losing your property if you can’t make the payments down the road. With that said, let’s take a look at the two phases of a Heloc. The first is known as the draw period, which is when you actually borrow the money. Like a zero equity product, you only make interest payments during the draw phase, with payments toward principal being optional. The draw period is typically 10 years.

The second phase of a Heloc is the repayment period, which is when you can no longer take out money and have to make both interest and principal payments. The typical repayment period is 20 years. Remember also that there are more expenses than just the interest that you’re being charged. Costs associated with the loan include closing costs, which contain things like property assessment values, attorney fees, etc. which can often run between 2% and 5% of the loan amount. Make sure you shop this around because each lender is different, with some lenders not charging closing costs at all. In addition, some lenders charge annual fees for Heloc customers, which are often around $50 per year. Not a biggie compared to closing costs.

So if you’re looking for a way to take cash out of your home without moving or refinancing at today’s higher rates, equity loan options are the ticket. According to Redfin, “Both home-equity loans and Helocs allow homeowners to keep the low rate they currently enjoy on their first mortgage, which in this market is an advantage.”