You may or may not be following the current crisis in the Middle East between Israel and Iran, but what you surely are following is how much it costs to fill your gas tank. With the peak summer driving season approaching quickly, Americans are likely to feel the pinch at the pumps as a result of politics thousands of miles away. Investing and Money told you months ago of the possibility of gold at $3,000 an ounce and oil prices over $100 a barrel. You may be jaded on oil if you own an EV and listen to non-stop MSNBC telling you how bad oil is for you and the world. However, you still need to get your head out of the sand and pay attention, even if you don’t care that oil could hit $150, and at those prices a global recession would be hard to avoid.

While Israel is not a significant energy producer, its strategic location and geopolitical importance make it a key player in the Middle East. On the other hand, Iran, a founding member of OPEC, produces approximately 3.2 million barrels of oil per day. Despite being under sanctions, any disruptions to Iranian oil production could still influence prices.

So how did we get here? Iran’s recent attack on Israel involved launching more than 300 drones and missiles from its territory. While the attacks caused minimal damage to Israel due to advance warnings, the situation remains tense. The price of Brent crude oil, the global benchmark, initially rose to a six-month high of $92.18 per barrel after the attack was anticipated. However, the destruction of most missiles led some analysts to believe that this might not mark the beginning of a prolonged conflict.

Despite the gloom and doom media coverage, why haven’t we seen a drastic move in oil prices to date as a result of the conflict? Several factors contribute to this restrained response:

- No Immediate Supply Disruptions: The attacks did not directly affect oil supply. OPEC members still have spare capacity to produce an additional 6 million barrels per day. If needed, they could use this capacity to drive prices down further.

- Hope for a One-Off Incident: Market participants hope that the attack remains an isolated event rather than the start of a full-scale war. This sentiment has kept prices from skyrocketing.

- Pressure on OPEC: The United Arab Emirates has already pushed for increased OPEC production quotas. If tensions persist and oil prices rise, further pressure may lead to adjustments in production levels.

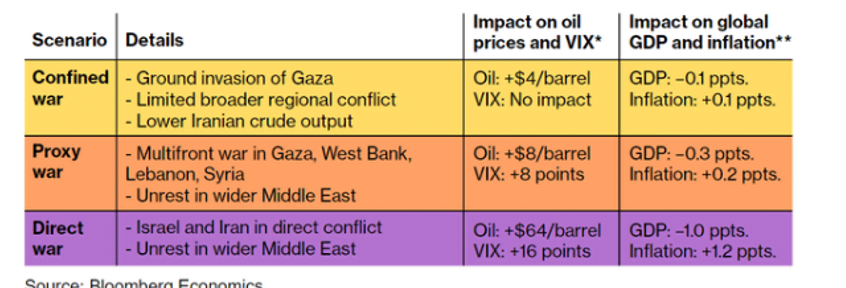

The effect on oil and other markets will obviously hinge on the Israeli response and the extent to which the conflict escalates, if at all. According to Michael Walden, Reynolds Distinguished Professor Emeritus at North Carolina State University, “Any ripple effects on gas prices depend on the countries’ next moves and whether they seek further retaliation against the backdrop of an already raging war.” In that regard, Bloomberg Economics has painted three scenarios and outlined the effect of each on the oil markets.

- The first scenario was a Confined War, where the “hostilities” remain in Israel and Palestinian territories.

- The second scenario was a Proxy War, where the hostilities spread to Lebanon and Syria.

- The third scenario was the Direct War between Israel and Iran.

The first two scenarios would have little effect in general. Oil prices would rise modestly and have little impact on stock market volatility, and still have no major effect on global inflation and growth. The third scenario is draconian and the one to pay attention too. A direct war could be expected to boost the price of oil by $64 a barrel, have a major effect on stock market volatility, cause an inflationary shock, and a global recession.

So what are those in the know saying currently? Citi raised its short-term oil forecasts to $88 per barrel from $80 on higher risk premium. However, Citi said it believes the current market is not currently pricing in a potential continuation of an all-out conflict between Iran and Israel that could push oil to $100 plus per barrel. Societe Generale said in a note that geopolitical risk is likely to become embedded in crude prices for the foreseeable future, and raised its Brent forecast to $91 per barrel in the second quarter and WTI to $87.5, and expects Brent to average $86.8 and WTI $83.3 in 2024.

If a direct conflict ensues, oil will go higher as a result. Israel is most worried about Iran’s nuclear program. Thus, Israel could decide to bomb Iran’s nuclear facilities. If this happens, Iran could be forced to attack the global economy by disrupting the flow of oil and this is the situation where oil spikes above $150, and the global economy slips into a recession.

While the recent attack did not immediately drive oil prices higher, the situation remains precarious. Investors, policymakers, and consumers must closely monitor developments in the region. The potential for further escalation underscores the need for energy diversification and robust contingency plans to mitigate the impact of geopolitical conflicts on oil markets.