The thought of investing in municipal bonds conjures up notions of a low risk, low return scenario, about as exciting as watching paint dry. Decades without inflation and uber low-interest rates have left this market in the dust.

However, the dust is starting to settle in muni-land and there may be an opportunity for you to get a piece of this tax-free income. You may not be the only one though. According to Refinitiv Lipper Data, municipal bond exchange-traded funds took in a record $1.8 billion for the week ended May 25, quadrupling their weekly average for 2022.

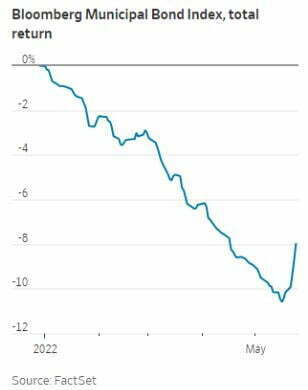

The chart below shows the dramatic slide in total return for municipals this year, with a recent pop that has possibly signaled a bottom. The roughly minus 8% return for munis in that period compares slightly more favorably than the overall U.S. Aggregate Bond index, which is down some 8.5% for the same period. “I think things are turning around. I don’t think it’s a blip,” Municipal Market Analytics partner Matt Fabian said of the rally. “I think munis had gotten too cheap.”

Municipal bonds are debt instruments issued by states, municipalities, or counties for the purpose of financing public capital expenditures, such as the construction of highways, bridges, and schools. The historic attractiveness of these fixed-income securities has been the tax-free nature of the interest income.

Although they may be tax-free, all munis are not created alike and are not by design totally risk-free. These securities are rated by credit agencies similarly to that of corporate bonds, giving them ratings from investment grade to high yield or junk.

Higher earners may find them particularly useful as a relatively low-risk way to limit their state and federal tax liability, while people with more modest incomes might look for investments that grow their overall wealth faster, even without the tax benefits.

Municipal bonds can be broken down into two main categories:

General obligation bonds

These bonds are issued by states, counties, and cities. They are not secured by any assets.

Instead, the bonds are backed by the credit of the issuer. If necessary, the state, county, or city can tax residents to get the money to pay back bondholders.

Revenue bonds

Unlike general obligation bonds, revenue bonds are not backed by the government’s taxing ability. Instead, they’re secured by the revenue from projects, like building highway toll booths.

As mentioned, munis are exempt from federal taxes, and if you live in the state or jurisdiction where the bond is issued you will be exempt from state and local taxes as well. However, just because these bonds are tax-free doesn’t mean that they will return more than a taxable bond. In order to compare apples to apples, you can use what’s known as the tax-equivalent yield, or TEY comparison. The formula is as follows:

TEY = tax-free municipal bond yield / (1 – investor’s current marginal tax rate)

For example, if an investor in the 35% tax bracket buys a tax-free muni bond yielding 4%, the calculation would go 4 / (1 – 0.35), and the bond’s TEY would be 6.15%. An investor would need to find a taxable bond yielding 6.15% to be comparable to this muni bond.

If you decide that munis have a place in your portfolio there are a few ways to get started. You can do the leg work and research and buy individual muni bonds. Muni bonds are typically a long-term investment, with maturities ranging from one to three years, and longer bonds ranging from 20 to 30 years.

If you hold a bond to maturity you don’t have to worry about volatility or price swings in the underlying bond, because you will get your investment back at par value on the date the bond matures. As with government and corporate bonds, laddering is a popular technique for diverse maturities of muni bonds. Depending upon your time horizon, you could invest in bonds that mature up until that point.

If you need the principal back in five years, for instance, you could ladder bonds that mature each year up until year five. You thought we might get through an investment piece without mentioning ETFs. The muni market is no different from other credit markets and offers exchange-traded products like ETFs as well as mutual funds. One benefit is accessing a well-diversified portfolio of bonds from municipalities with different credit ratings, a range of projects and bond types, and varied risk and return.

This lessens any potential default risk as you spread your dollars across many bonds.

Although the bleeding in the municipal bond market has appeared to stop, many remain leery of the market for the near future. According to Mikhail Foux, head of municipal strategy at Barclays PLC, “Economic turbulence, volatile bond rates, or more bond issuance than expected could push prices downward. The market is not out of the woods as of yet.”

Caveat emptor.