They grew up with Woodstock and the civil rights movement, and now they’re the wealthiest generation in history. The baby boomers have accumulated some $30 trillion in wealth, and their financial planning choices could change the course of wealth management. While in mass the boomer generation is on track to leave the largest financial legacy in history, but individually their legacy planning could be unique. Luis Carlos De Noronha Cabral Da Camara, a wealthy Portuguese aristocrat, left his entire fortune to seventy strangers he found in a Lisbon phone book. Jack Benny, the popular comedian, used a portion of his wealth to deliver his wife a long-stemmed rose every day for the rest of her life. So what are the ways that this iconic group will leave a lasting legacy?

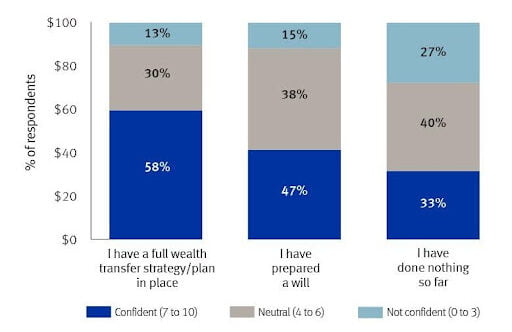

Although quite large in number, the vast majority of baby boomers are not totally prepared to pass on their accumulated wealth. This was highlighted by the somewhat recent death of music legend Prince. While a millionaire many times over, he never even created a will. And he’s not alone. It is estimated that only 54 percent of high net worth individuals have a will, and while 26 percent said they have a wealth transfer plan in place, another 32 percent said they had done nothing yet to prepare. One has to wonder why this is so. “For the boomer generation, you didn’t talk about money—money was generally a taboo topic—so I think that’s still playing into the culture,” says Angie O’Leary, head of wealth planning for RBC Wealth Management.

If you are so inclined to prepare a wealth transfer you should consider things like what you value in addition to just thinking about dollars. The broad brush categories that initially come to mind are things like charitable contributions and education. For example, if education is a significant value, you might create 529 plans for your grandchildren. Clarifying your values and goals can also be helpful for the next generation, particularly if inheritors feel unprepared or overwhelmed. O’Leary points to the example of a client who had received a sizeable inheritance six months earlier and didn’t know what to do with it. An inheritance can often times be somewhat like a new born baby, in that it doesn’t come with instructions. The inheritor often has no idea what to do with a large sum of money, so it can be a nice touch if there is a value message associated with it.

Leaving a family legacy might also include gifting money away from the family itself. Individuals may have philanthropic goals that drive their charitable contributions, desiring to leave money to causes and organizations that are most important to them. According to Penn Mutual Company, an investor can set up what is known as a donor-advised fund, which is a quick and tax-efficient way to make a charitable impact. Features of such funds include:

- Tax-deductible deposits in the year contributions are made

- Flexibility to make grants immediately or schedule well into the future

- Initial deposit as little as $5,000 to get started

The dynamics of your family can play a part in how you determine to transfer wealth. You may have children with special needs or specific health issues that you may want to address in an inheritance. If you had a child with Type 1 diabetes for example, you may want to set up a fund so that the child may have medical care for the foreseeable future. Another common occurrence involves that of a second property or family vacation residence that has sentimental value. If you have multiple heirs with differing opinions on the property you will want to take these factors into consideration. One option would be putting the property in a trust with dollars to support the maintenance of it, or setting up a qualified personal resident trust where you pick the term of years you live there before it transfers to your kids.

In regard to leaving a financial legacy, you don’t necessarily have to have a high net worth. According to financial planner Thomas Sagissor, “No matter your net worth, you can leave a financial legacy to your children, and that legacy can have an incredible impact on their financial future,” says Sagissor. “I know families who didn’t have a lot of extra money who taught their children the value of saving every penny they earned and never spending more than they have—which is creating a financial legacy. If you’re thinking about ways to create your legacy for your family, don’t wait. Time is a valuable commodity, and the sooner you start, the better.