So you may have been asking yourself why am I still receiving no interest on my bank savings accounts with interest rates rising and the Federal Reserve set to tighten the screws even more. Well, that is a question for another day, but simply put savings rates always lag government led rate increases, and you the investor will always be behind the rate curve. But do not fear.

We can help you boost your anemic returns with the help of your tax refund and with a government guaranteed rate of return. And yes, that is the U.S. government, and not some banana republic that will pay you in meme coins.

We’re speaking of course of Series I Bonds. If you’re unfamiliar with them, a series I bond is a non-marketable, interest-bearing U.S. government savings bond that earns a combined fixed interest rate and variable inflation rate (adjusted semiannually).

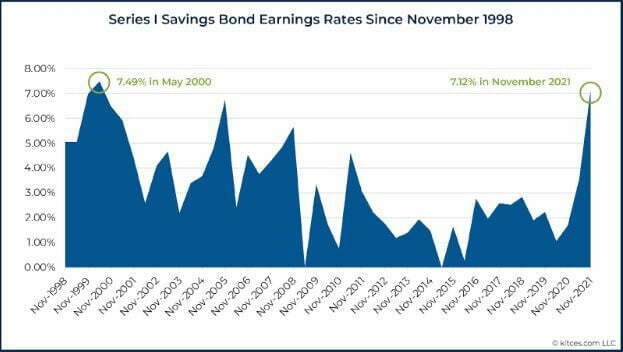

Series I bonds are meant to give investors a return plus protection on their purchasing power. This sounds just like what the inflation doctor has ordered. The following chart depicts a graphic illustration of the power of these bonds during inflationary times.

Yes. It sucks that inflation is rearing its ugly head and increasing the prices of goods and services across the board. In an attempt to somewhat mitigate this effect, the government created investment vehicles to allow you to offset inflation with additional alpha so to speak. Otherwise known as “I bonds,” these virtually risk-free investments already have a lot going for them, including that they’re backed by the U.S. government, their value doesn’t go down, they offer tax benefits and, perhaps most appealing, they are set to pay more than 9.6% in interest a year.

Let’s take a look at some of the key points of these investment bonds. First, one must note that individuals can’t buy I bonds through a brokerage account, only through the U.S. Treasury Department’s website, and there is a limit to how much you can invest.

You generally can’t buy more than $10,000 in I bonds each year, plus an optional $5,000 extra if you put your tax return in paper bonds. We’ll go into a little more detail on how the tax refund works in a minute. Also of import is the duration of these bonds.

I bonds mature after 30 years, meaning you can continually earn interest on them for 30 years unless you cash them out first. As with other types of savings bonds there are penalties for early withdrawal. While you can redeem them as early as one year after your initial purchase, cashing in early, specifically within five years, means you forfeit the last three months of interest earned.

So, like a Roth IRA, make sure that this is something that you can hold on to for at least five years to avoid paying penalties. Also, like the IRA, you can defer declaring your interest until maturity or when you cash out, effectively allowing your investment to compound tax free.

According to Adam Hayes, CFA and PhD in Economics from The University of Wisconsin-Madison, there are several key takeaways that you will want to be aware of:

- Series I bonds give investors a return plus inflation protection on their purchasing power and are considered a low-risk investment.

- The bonds cannot be bought or sold in the secondary markets.

- Series I bonds earn a fixed interest rate for the life of the bond and a variable inflation rate that is adjusted each May and November.

- These bonds have a 20-year initial maturity with a 10-year extended period for a total of 30 years.

Let’s go back and look at how these bonds tie in with taxes. Oddly enough, the IRS has a form relating to an inflation play for savings that some late filers still have time to consider. If you file by this years’ regular deadline of April 18th, taxpayers can file what’s called Form 8888 to use at least part of their federal income tax refund to directly buy I Bonds when they’re filing their federal tax returns.

Perhaps this tip is relatively unknown, since according to the IRS only 128,783 paper Series I savings bonds, totaling about $31 million, were issued as of March 31 as part of tax refunds. It could be that from a wealth management perspective, high net worth investors are considering if an I bond makes that big of an impact on their overall portfolio, given the $10,000 maximum limit.

If this is a considerably small amount, it probably doesn’t make sense to open one.

A final point of note to consider is the comparison of I Bonds to Treasury Inflation-Protected Securities (TIPS). I think the choice is really one of portfolio size. While both securities protect your principle and purchasing power, the amount one can buy is markedly different. As mentioned, individuals can only buy $10,000 worth of I Bonds in a single calendar year, while $5 million in TIPS can be purchased at any single auction.

In addition, you can sell TIPS anytime you want in the secondary market, but you can’t sell I Bonds for at least a year after purchase. TIPS can be bought for various terms, and I Bonds earn interest for 30 years.

If either of these inflation-protecting investments interests you, you can purchase TIPS, for instance, online through TreasuryDirect or from a bank or broker, while you can only purchase I Bonds online at TreasuryDirect. At least you can find a little ray of hope in this inflationary environment.