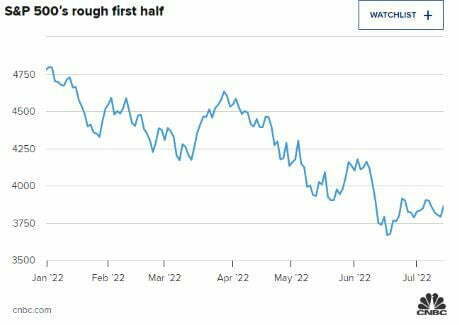

If you’re like most investors you probably want to forget about the first half of 2022.

The benchmark S&P 500 had its worst first six months since 1962 and the worst June since 2008, closing down the month some 7.58%. If you think it was about stock picking you’d be wrong. According to Howard Silverblatt, Senior Index Analyst at S&P Dow Jones Indices, all 11 sectors of the S&P were down, with only 53 issues up and the remaining 449 down.

The dismal trail continued on through Q2 2022, where the S&P 500 dropped 18.87%. Last 4th of July, investors were opening their half-year statements with a 15.70% gain, now it’s a 19.88% decline. There is perhaps a silver lining if history is to repeat itself. When the S&P 500 plunged 21% in the first half of 1970, it promptly reversed those losses to gain 26.5% in the second half.

As democratic pundit James Carville put it, “It’s the economy stupid.” And to drill down a bit more, its inflation, plain and simple. A couple key points behind inflation we need to keep an eye on are:

- How consumers react to inflation (this week’s Consumer Confidence level was, in a word, terrible, a 16-month low), even as they spend through the summer

- If the expected two 0.75% FOMC interest rate increases (July 27 and September 21) permit a pause

- If (overall) inflation data plateaus

Just like in 1970, the stars have to align again to pull of that kind of comeback. Quincy Krosby, chief equity strategist for LPL Financial, puts it this way, “You trade and invest in the markets you have, not the ones you want,” Krosby said. “Can this market recover in the second half? A lot has to be lined up. But it’s happened before.”

We know that growth stocks generally thrive during periods of economic expansion when interest rates are low. This is exactly the scenario that’s transpired since the financial crisis of 2008, where growth stocks massively outperformed the Graham and Dodd value stocks and the S&P 500 Index as a whole.

If you want to bet on a comeback play similar to the one we mentioned into 1970, then perhaps these lower valuations on growth stocks might be a possible buying opportunity. Here are several that you may want to consider.

Vertex Pharmaceuticals Inc. (VRTX)

3-Year Annualized EPS

+3.7%

3-Year Annualized Revenue

+35.5%

Return on Equity

24.7%

Vertex reported 22% product revenue growth in the first quarter, including 47.7% sales growth of lead drug Trikafta. Bank of America analyst Geoff Meacham projects $7.25 billion in Trikafta sales in 2022 and says VRTX’s additional drug candidate pipeline provides an “intriguing mix of potential new growth drivers.”

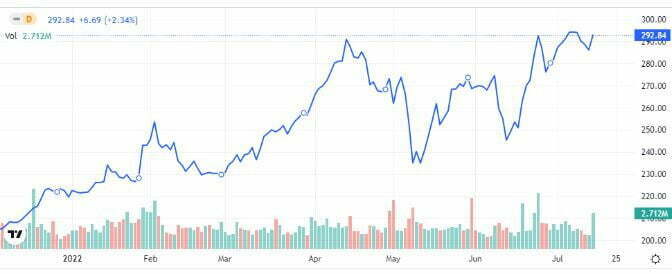

TransDigm Group Inc. (TDG)

3-Year Annualized EPS

-13.7%

3-Year Annualized Revenue

+7.9%

Return on Equity

N/A

While the revenue and EPS figures may not be that impressive for the last three years, the company believes that its aircraft parts business will begin to grow again post Covid. In the fiscal second quarter, TransDigm reported 11.1% revenue growth, 15.1% organic revenue growth, and 91.3% net income growth.

In addition, the company has a stock buyback plan whereby they repurchased $667 million worth of shares last quarter alone. Bank of America has a “buy” rating and a $765 price target for TDG.

T-Mobile US Inc. (TMUS)

3-Year Annualized EPS

-10.4%

3-Year Annualized Revenue

+22.7%

Return on Equity

4.1%

The way that T-Mobile spends on television advertising would make you think that they plan on increasing its EPS from its negative 10.4% rate of the last three years. The ongoing integration of the 2020 Sprint acquisition should be a continued EPS driver going forward. In addition, their 5G network is helping gain market share in small and rural markets. The stock has a consensus buy rating with a $155 price target.

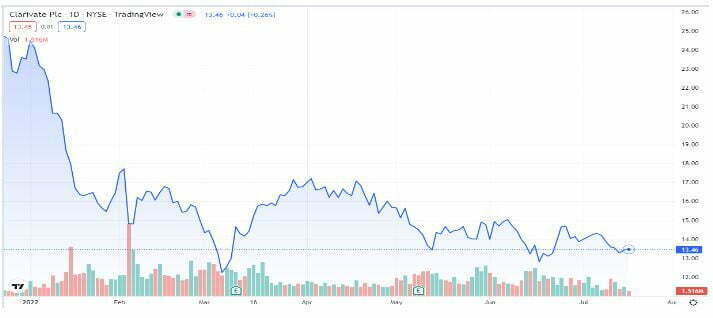

Clarivate (CLVT)

- Market value: $10.0 billion

- Dividend yield: N/A

- Analysts’ ratings: 3 Strong Buy, 3 Buy, 2 Hold, 0 Sell, 0 Strong Sell

While not an everyday name that most have heard of, Clarivate is a global information and data analytics company. It helps more than 50,000 customers in over 180 countries obtain the information necessary to make informed decisions about their organizations and businesses. You can’t ignore the financials, with free cash flow really catching my eye. Clarivate expects to generate revenue and adjusted free cash flow of $2.84 billion and $700 million, respectively in 2022.

In 2023, it expects revenues of approximately $3.0 billion and more than $800 million in adjusted free cash flow. The stock price has been cut in half since the first of the year, so this may be a bottom worth averaging into.

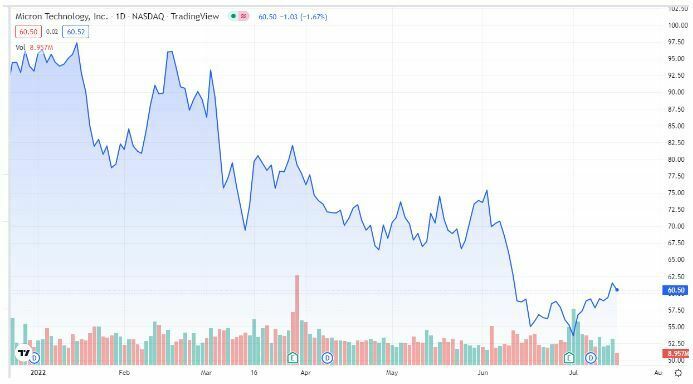

Micron Technology (MU)

- Market value: $65.6 billion

- Dividend yield: 0.7%

- Analysts’ ratings: 24 Strong Buy, 6 Buy, 4 Hold, 1 Sell, 0 Strong Sell

The semiconductor market has been hit hard this year with, among other things, issues in the global supply chain weighing heavily on it. As such, continued skepticism from analysts have resulted in a nasty price haircut for Micron this year. However, even with the recent downgrades, the vast majority of covering analysts still rate MU stock a buy. They also have an average target price of $97.45, well above the current share price.

Patience is a virtue here, with the belief that semiconductors are a strong bet for the future, as their use will continue to grow with the ever-increasing demand for data and increased storage and processing speed.