The one thing that the average American can count on is that they will feel the effects of the last Federal Reserve move and the fallout from the banking crisis in a way that will make life more expensive.

Unless you were lucky enough to be one of those uninsured by the FDIC, ala Roku and Silicon Valley et al., to get bailed out (by your tax dollars, by the way), you will probably feel the financial pinch at every turn.

The argument offered by the government to you, which is at least better than saying, shut up and don’t ask questions, as is the norm these days, is that by bailing out the likes of SLV and Signature Bank, it will avoid contagion to other regional banks and even eliminate a possible run on banks. Yes, it’s 2023, and we’re talking about the possibility of banks not having your money when you want it.

The demise of regional banking is far from over.

Last month shares of PacWest bank are down about 11% on the day as the bank just issued a report that stated their total deposits have decreased. That’s a nice way of saying people are taking their money out. Although some 65% of total deposits at PacWest are FDIC insured, the bank wasn’t liquid enough to meet these deposit withdrawals.

The bank cited market volatility, depressed regional bank stock prices, and alternative funding options as reasons for borrowing funds from the Federal Reserve. Regional banks are the backbone of lending across America.

How easy would it be today to walk into a PacWest branch and ask for a car loan? Now you’re seeing how this all trickles down to your wallet.

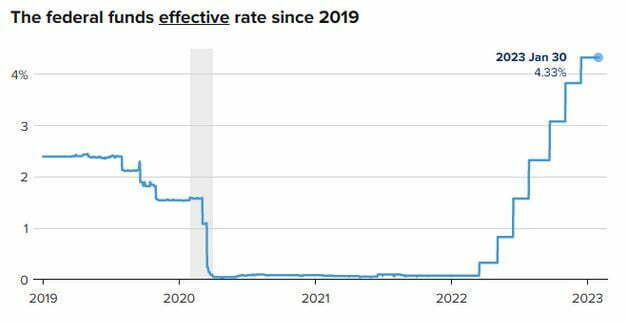

The Federal Reserve raised interest rates by a quarter point at the March meeting and is expected to raise rates again this year. However, the recent troubles mentioned above, caused in part by higher rates, will lead banks to toughen lending standards across the board regardless.

According to Timothy Chubb, chief investment officer at Girard, a wealth-management firm, “Banks will likely be more conservative with who they are lending money to in this environment.”

How does this impact you?

The raised restrictions would make it harder to get a car loan, mortgage, or small business loan. According to economists at Goldman Sachs Group Inc, the tougher standards would be equivalent to a quarter or half-point increase in the Fed’s benchmark rate.

The following chart depicts the federal funds rate since 2019.

For consumers, that means they must still pay a higher price to borrow while grappling with a persistently high cost of living.

Tomas Philipson, a professor of public policy studies at the University of Chicago and a former acting chair of the White House Council of Economic Advisers, says, “They [consumers] are right in feeling these are dire economic times. It’s not how many dollar bills you have, it’s what you can buy with them.”

With the cost of living increasing via higher inflation and the higher cost of debt financing, what can you do to mitigate this financial hardship?

Here are a couple of strategies to consider:

Lower your Credit Card Debt

Just about every credit card has variable interest rates, which means that as the federal funds rate rises, the prime rate increases, which raises the rate on your credit cards.

After a prolonged period of rate hikes, the average credit card rate is now over 20%, an all-time high, up from 16.34% one year ago. The math does not bode well for borrowers.

According to Matt Schulz, chief credit analyst at Lending Tree, “Someone with $5,000 in debt on a card with a 23.65% APR and a $250 monthly payment will pay about $1,277 in interest and need 26 months to pay off the balance.” If you can’t pay down your credit cards, you might consider a balance transfer to another card or a lower-interest personal loan.

Shore up your Credit

It’s always hardest on those who have poor credit in times of rising interest rates. Not only will it be more difficult to obtain credit, but the cost of borrowing will also be more significant.

Arthur Weissman, the co-founder of Industry FinTech, a financial-services company, says, “Try to reduce your credit-card debt to below 50% of your available credit, pay your bills on time and clean up any issues on your credit report.”

Check your credit score to track your progress. Financial advisers say that even minor improvements to your credit score can make a difference in the cost of getting a mortgage.

Maximize your Savings

As most of you know, you have received virtually no interest on your bank savings for the last decade as interest rates have hovered around zero.

While the Fed has no direct influence on deposit rates, the rates tend to be correlated to changes in the target federal funds rate. According to Bankrate, the dramatic increase in the federal funds rate over the last year has seen top-yielding online savings account rates go as high as 5% plus, much higher than last year’s 0.75% rate.

The recent turmoil in the banking sector shouldn’t fear the average American. Remember, the FDIC insures bank balances for up to $250,000. People with balances greater than $250,000 should make sure their funds are FDIC insured by spreading their savings across different banks or employing other strategies.