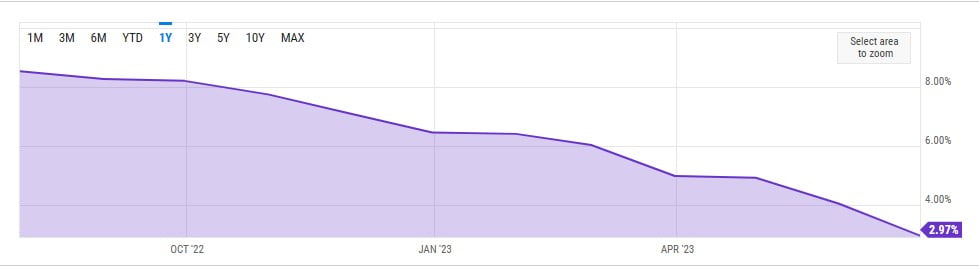

There may be a silver lining in the recent interest rate hikes by the Federal Reserve. That silver lining comes to investors in the form of making more money on their savings accounts. If you bank with a traditional brick-and-mortar lender you may not have noticed, but anyone who watches TV knows that online banking institutions are waving high-interest savings accounts to consumers. The U.S. inflation Rate in June was at 2.97%, compared to 4.05% last month and 9.06% last year. This is lower than the long-term average of 3.28%.

Online banker CapitalOne, among others, is currently offering a savings account with no minimums or fees with an interest rate of 4.3%, which nets you about 1.3% above the June inflation rate. The following chart show rates from last June’s high to the current month.

The Fed raised short term interest rates by 0.25% on Wednesday, the latest in a rapid series of increases that have brought rates from zero in early 2022 to a target range of 5.25% to 5.5% now. The federal funds rate hasn’t been this high in 22 years. With that said, what goes up will likely go back down. Since 2012, the Federal Reserve has targeted a 2% inflation rate for the U.S. economy and may make changes to monetary policy if inflation goes back within that range.

The flip side of the inflation coin is a recession. If the Fed believes that they have inflation under control, they won’t want to continue tightening so much that it pushes the economy into a recession. That means that it could become a lot harder to find savings accounts and certificates of deposit paying the most attractive rates. “I think we’ve already broken past the peak,” says Sander Read, a financial advisor in Winter Park, Fla.

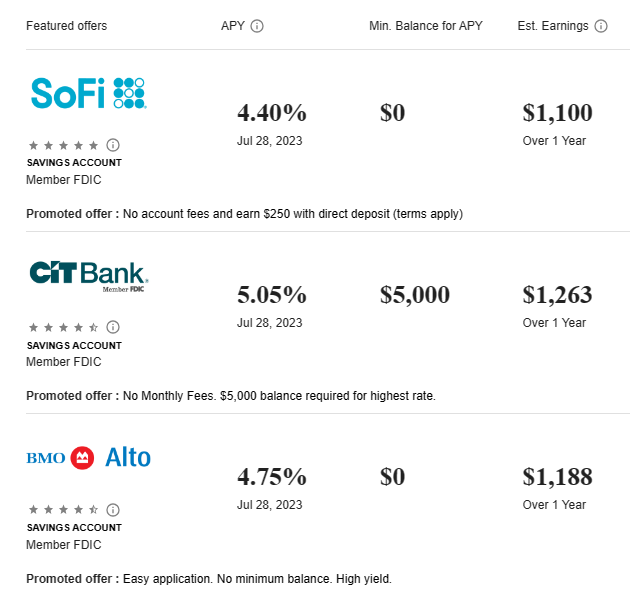

So what should you do with your savings? It really depends on your time frame and when you’ll need the money. If you generally plan on needing the money within a year, a high yield savings account is probably a better option than locking into a CD. I mentioned CapitalOne as one of the online banks that is providing rates that currently beat inflation. A couple of others include the following.

If your time horizon is greater than a year, CDs are one of the best ways to go. Currently, you can find FDIC insured CD’s yielding a tad more than savings. The best one year CDs are yielding more than 5.25%, with two and three year CD’s paying a fraction more. You can look at the equivalent bond yield to get an idea of what CDs will pay. According to investment advisor Brian Frank, in Key Biscayne, Fla., “Whatever the three-year government bond is yielding, [similar three-year] CDs should be yielding a bit more.”

In addition to the CPI inflation number mentioned above, the Commerce Department released its personal consumption expenditures price index Friday, which was just 0.2% higher than the prior month, but up 4.1% from the year before. This is an inflation gage that the Fed watches closely and is used to help decide whether additional inflationary rate hikes are needed. According to George Mateyo, chief investment officer at Key Private Bank, “Today’s economic releases reaffirm the current market narrative that inflation is cooling and economic growth is continuing, which is a favorable environment for risk assets.”

If you have an investment account with someone like TD Ameritrade or Fidelity, you most likely have a money market account or a money market fund, where cash is stored to obtain liquidity if not needed for investment. The caveat here is that, unlike many other savings account alternatives, money market funds aren’t FDIC insured. Although these instruments are designed to be extremely stable, they are not risk-free or guaranteed by the government.

Finally, you could go to the risk-free source itself, government treasury bonds, notes, and bills. A few stats and key statistics sum these up well.

- Backed by the full faith and credit of the U.S. government

- Purchased through TreasuryDirect or secondary market

- Minimum purchase amount through TreasuryDirect: $100, sold in $100 increments

- Current yield on the 2-year Treasury note is roughly 4.5%

- Current yield on the 10-year Treasury note is roughly 3.7%

- Current yield on the 30-year Treasury bond is roughly 3.9%

- Interest income is exempt from state and local taxes

Remember that financial advisors will want to know about your liquidity needs and your risk tolerance, among other things, and will usually steer you to an approach that doesn’t put all your liquid cash in one vehicle.

For example, you might keep a portion of your emergency savings in a money market account or a high-yield savings account, and the remainder in a series of CDs or bonds laddered to mature at regular intervals in case you need to start drawing down your savings in the event of a job loss or other financial crisis. Regarding risk, just make sure that your account is either FDIC or NCUA insured.

If you’re not sure, just ask!