As of this writing the U.S. dollar is still the reserve currency for the world, and despite being knocked down a peg or two by rating agencies, world banks, and others, it looks like it will remain the defacto world reserve currency for some time to come. Now that we’ve established the dollar as the all-mighty currency, we need to take a look at its current rally against the euro and other major currencies, and more importantly for you, how this dollar strength is going to impact the equity and debt markets going forward.

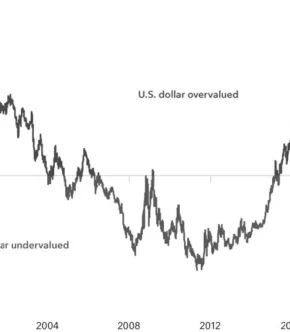

First off, how do you price the dollar and what factors influence that price. As is much of economics, price of the dollar is dictated by supply and demand. The more demand for the dollar, as we are seeing in recent months, will push the price higher, all other things, including supply, being equal. According to Rob Haworth, senior investment strategy director at U.S. Bank Wealth Management, “Relative currency values reflect the global flow of funds. When the dollar strengthens, it means more foreign money is flowing into the U.S. than the other way around.” Pretty basic, right? The following chart shows the price of the U.S. Dollar Index year-to-date.

After weakening earlier this year, the U.S. dollar is pushing higher and could be headed back toward the 20-year high it touched in 2022. That hasn’t always been the case. As recently as 2008, it took nearly $1.60 to purchase the equivalent of one euro. The dollar recovered some ground in August and September of 2023, moving up to just under $1.06 to the euro.

The dollar recovered from that point, but with a great deal of fluctuation in value along the way. So what’s caused the change? Very simply, the Fed. The interest rate environment, dictated by the Fed, and the monetary policy that encompasses it set the table for where we are today. The Fed’s decision to raise the federal funds rate quickly prompted other bond yields in the U.S. to move higher relative to other foreign debt instruments. As such, real yields tended to draw more foreign dollars, and this demand drove the value higher.

Even if you aren’t planning on traveling to the south of France or the Greek Islands any time soon, the prospects of a stronger dollar can still benefit you. A positive feature of a stronger dollar is the lower cost of imported products from other countries. Thinking about buying that new euro motors BMW or Mercedes this Christmas? A stronger dollar may help. If a car made in Germany is valued at €50,000 and then is imported to the U.S. when the dollar stands at $1.20 to €1, the retail price of the car in the U.S. would (theoretically) be $60,000 (20% more than its European price to reflect the currency exchange rate). If the dollar were to appreciate to $0.90 to €1, the car’s value in the U.S., using the same assumptions, would decline to $45,000, a significant savings for a U.S. consumer.

What can be an advantage to the consumer comes at a cost for corporate America. A strong dollar can detract from the revenues generated by U.S. companies. A stronger dollar means U.S. companies that export products abroad will be less competitive because the price of the product translated into euros or another currency is higher, which can lead to lower sales as foreign buyers shift to lower cost alternatives. According to Gian Maria Milesi-Ferretti of the Brookings Institution, “If you’re outside the U.S., there is basically one upside to a strong dollar: U.S. consumers and companies have money that goes farther, so they can buy more of what you’re selling.”

With that said, a strong dollar is filled with downside. Start with the fact that many governments and companies borrow in U.S. dollars. The cost to service debt rises with a stronger dollar, as well as making it harder to get new loans in dollar terms. You’re not the only one who has noticed that you’re now receiving more interest on your savings dollars. On the foreign exchange front, one could borrow money at nearly 0% interest in Japan, and invest it in short term CD’s or treasury bills and earn a positive yield on the arbitrage.

So how does this stronger dollar affect your investment decisions regarding equities? In the longer term it really shouldn’t. According to Haworth, “The impact of currency movements shouldn’t be a major consideration for investors as they assess the value of specific stocks.” Currencies are less volatile than stocks as a whole, and their direction, like that of the market, is difficult to predict. The situation is different if you are looking to invest abroad or in emerging markets. Consider the value of an investment in the MSCI European Union (EU) Index. In 2022, the index, in local currency terms, generated a return of -14.13%. However, the net return for a U.S. based investor in the fund, translated back into dollars, was -19.97%. In other words, the strong dollar detracted from the return. Again, it can be beneficial to account for currency risk if your portfolio has international exposure, but on a domestic front investment decisions really shouldn’t be made on currency risk only.