In today’s real estate market one has to think outside of the box in order to make a financially sound decision when purchasing or selling a home. The real estate market has changed, as we’ve outline recently on Investing and Money. From the mammoth National Association of Realtors settlement to decade high interest rates, it takes a financial Magellan to navigate the home buying and selling process today. With that said, the metrics behind financing property don’t change, just the numbers used to calculate them. When determining your monthly mortgage payment, the variables are the rate of interest and the duration of the mortgage, or simply put, how many years are you going to finance the property. The typical mortgage as most know is calculated over 30 years, for the simple reason that the amount being financed is large in comparison to the income typically needed to pay it back. Thus, the longer the duration of the mortgage, the lower the monthly interest and principal payment will be.

So how does one decide on the duration of a mortgage loan? Well, it typically is decided for you by your bank or lending institution, who in the past have offered very few options in terms of duration, with 30 year and 15 year loans being the norm. With the advent of non-bank banks and other non-conforming lenders, the options available to borrows today have increased, with loans that can range in duration from as short as five years to as long as forty years. Countries like Japan actually have loans that extend out to almost one hundred years, mimicking the lifespan of the owner. According to Fannie Mae, in 2021, 70% of new mortgage loans were for a 30 year fixed-rate term and an additional 9% were 15 year fixed loans, with others such as 10 or 20 years, making up just 10% altogether.

One has to be careful when locking into a shorter term duration mortgage. While it’s enticing to see how much faster you can pay down principle and get out of debt, the larger monthly payment can turn into a strangle hold if your finances change. The reason you would typically get into a 15 year loan over making additional principle payments to a 30 year loan is that the interest rate is usually lower on the shorter end, meaning you’d likely get a lower interest rate on a 15 year loan as opposed to a 30 year loan. The yield curve today is inverted in the short term durations, but a 30 year mortgage will still cost you more than a 15 year.

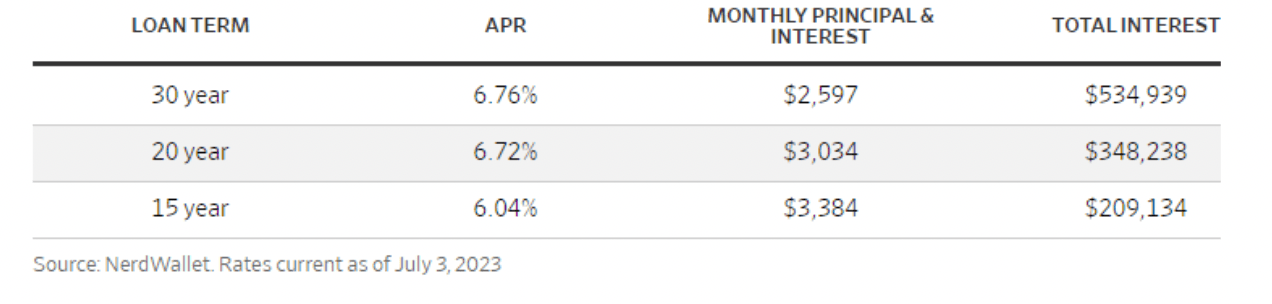

Take a look at the term options if you were oscillating between a 15, 20, and 30 year mortgage. If you want to compare 30, 20 and 15 year fixed-rate loans today, here’s an example for a $400,000 loan:

So now that you’ve figured out how long of a mortgage you want to carry, how about the down payment. This is typically what keeps most from home ownership. Even 5% down on a $200,000 home is $10,000, often out of reach of the average American, considering that 60% of people in the U.S. don’t have an extra $1,000 to cover an emergency expense.

Believe it or not there is a government program that will allow you to finance the term structure of your desire with no money down, and it’s called the USDA. Who would have thought that the United States Department of Agriculture was in the mortgage game, and especially the no-payment down one? As you might imagine, there are a few caveats here that make the average American either unable or undesirable to assume one of these loans.

If you’re like me and had never heard of these USDA loans you’re not alone. According to NerdWallet, only 118,000 home buyers used a USDA loan in 2022, accounting for a very small portion of the over 16 million loans issued that year. Furthermore, you generally must be willing to live in a rural or remote location to get access to these no down payment loans. According to Mike Roberts, co-founder of City Creek Mortgage in Draper, Utah, “Home buyers with modest incomes and those craving the peace and quiet of countryside living are ideal candidates for USDA loans. They’re also a great fit for first-time buyers who might not have substantial savings for a down payment.”

There are two main types of USDA purchase loans: Guaranteed loans and direct loans. Guaranteed loans are mortgages that are issued by private lenders, but the USDA guarantees them. Direct loans are mortgages issued by the USDA itself and are only available to borrowers with low or very low incomes compared with the area median.

It’s a very interesting and anxious time in the current history of the real estate market. Higher relative interest rates, albeit the real possibility of paying lower real estate commissions, keeps all parties on their toes. Think about a shorter duration mortgage like the 20 year if it makes sense, and if you have a hankering to live off the grid, give the USDA no down payment loan a look.