Higher Interest Rates Could Push U.S. Off the Cliff in Next Decade

When it comes to unraveling our republic it may not be in the manner that you were thinking of. It seems like just yesterday that radical Islam and their chants of Allah Akbar and death to the west was the most pressing issue to our survival as a nation. The enemy within is near the top of the list today, wreaking havoc on the republic as we knew it. The last 40 years have brought us to the point of a nation divided 50/50, which will not bode well for the future of the country if we remain in such divide. But perhaps the most existential threat to our survival is more esoteric, not taking sides in the cultural wars or politics in general. But you know what it is. As we’ve said here in Investing & Money many times, just follow the money and you’ll find the answer.

So what are we talking about boys and girls? Money, of course, or in this case, the lack of it. There’s a little known codicil that keeps getting larger each day that threatens America’s financial sovereignty as the word’s bellwether leader. We’re talking about the federal debt or deficit of course. Quite an intro for something so bland and seemingly benign. But this silent killer has the capacity to render the U.S., and the dollar in particular, incapable of supporting itself. That’s a pretty bold statement considering we have the largest economy in the world, and that you’ve heard nothing about it in this election cycle. Let’s look at some of the numbers behind this draconian scenario.

Current Situation:

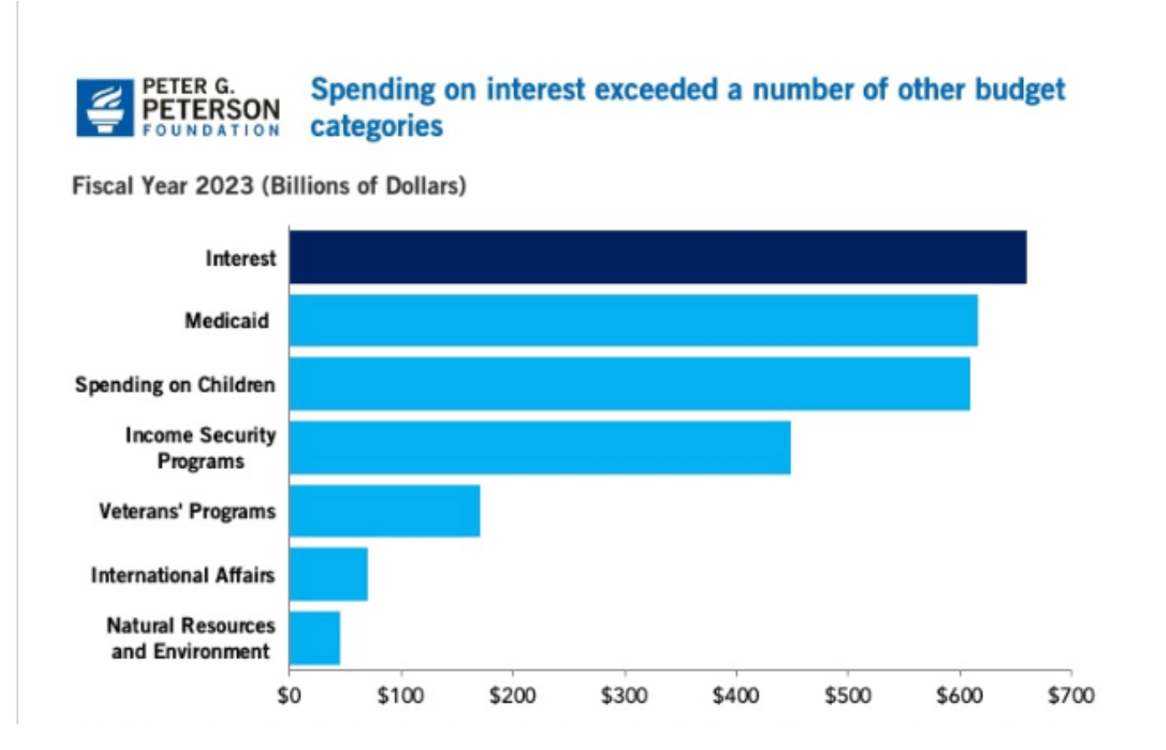

- In 2023, interest costs on the national debt totaled $659 billion, surpassing most other components of the federal budget.

- The Congressional Budget Office (CBO) projects that interest costs in 2024 will reach $870 billion, representing a 32 percent increase from the previous year.

- These high interest payments are part of a trend that extends into the future, driven by growing debt and relatively high interest rates.

We’ve cited the Penn Wharton Budget Model here before, and it’s worth repeating some of its findings. According to Penn Wharton, The U.S. “public debt outstanding” of $33.2 trillion often cited by media is largely misleading, as it includes $6.8 trillion that the federal government “owes itself” due to trust fund and other accounting. The economics profession has long focused on “debt held by the public”, currently equal to about 98 percent of GDP at $26.3 trillion, for assessing its effects on the economy.

To put the CBO’s interest costs of the debt in perspective, the following chart shows it in comparison to other categories of government spending.

So what happens if rates continue to rise? The cycle looks something like this:

- When the U.S. government borrows money by issuing Treasury securities (such as Treasury bills, notes, and bonds), it pays interest to the investors who hold these securities.

- The interest rates on these securities are influenced by various factors, including the Federal Reserve’s monetary policy, market conditions, and economic outlook.

- Higher interest rates mean that the government must pay more to service its debt, increasing borrowing costs.

Over the next decade, the U.S. government’s interest payments on the national debt are estimated to reach a staggering $12.4 trillion, more than double the total spent in the past two decades. If interest rates rise by 1%, we can expect even higher costs. For every percentage point of increase, the additional expense would be $8.7 billion. Even small changes to national interest rates as mentioned can lead to significant changes in public debt interest payments. If rates rise to a single percentage point above the CBO’s estimates for the next several years, it could mean that the U.S. will spend more on interest payments than national defense by 2029. That’s pretty staggering, considering we’re getting nothing to show for it.

To carry out that scenario a bit further, the CBO projects that net interest costs will eventually become the largest “program” in the federal budget, exceeding Medicare in 2046 and Social Security in 2051. Rising interest costs also contribute to a vicious cycle of higher debt and additional interest costs.

Let’s circle back to the Penn Wharton budget model to see what options may be available. First off, the Penn Wharton forecast assumes best case scenario that we melt down financially from the budget deficit in 20 years. Any type of event that would alter the markets could significantly reduce that 20 year estimate. According to Penn Wharton, “Forward-looking financial markets are, therefore, effectively betting that future fiscal policy will provide substantial corrective measures ahead of time. If financial markets started to believe otherwise, debt dynamics would “unravel” and become unsustainable much sooner.” Alternative paths to avoid this financial crisis include:

- Raising taxes on corporations and high-income households.

- Broad-based changes to Social Security, Medicare, and the employer deductibility of health care.

- A mix of new tax revenues (including a carbon tax and a value-added tax) along with discretionary spending cuts.

Any and all of those tactics mentioned will work, but only if we have the political will to stomach them. The first bullet point is right out of the DNC talking points paper. Raise taxes et al. There you have it. The second bullet point has been kicked around since I was in business school in the 80’s. Everyone knew then what they know now, however the can just keeps getting kicked down the road for future generations to solve/retain the problem. Imagine if only a small percentage of social security and the entitlement funds had been invested in America via the S&P 500. We would be surplus cash by the billions and this discussion would be moot. You can blame those that don’t trust Wall Street or capitalism for that then, just as they are telling you that it’s evil now. Don’t listen to them.