Talk about a reversal of fortunes.

One could do no wrong as a homeowner in the last five to ten years. Buoyed by low-interest rates, heavy demand, and lack of products, prices and equity skyrocketed.

Throw in a pandemic in 2020, which fueled the desire to flee certain locations for others, and you had created a massive bull market. What a difference a year makes.

Enter the world of 2023 with high inflation and interest rates, and you have a total turn of events. Like just about every other sector of the market these days, it is all about the Fed. According to UPenn Wharton professor Susan Wachter, “The Fed is using the housing market as a fulcrum to slow overall activity and get the inflation rate down.”

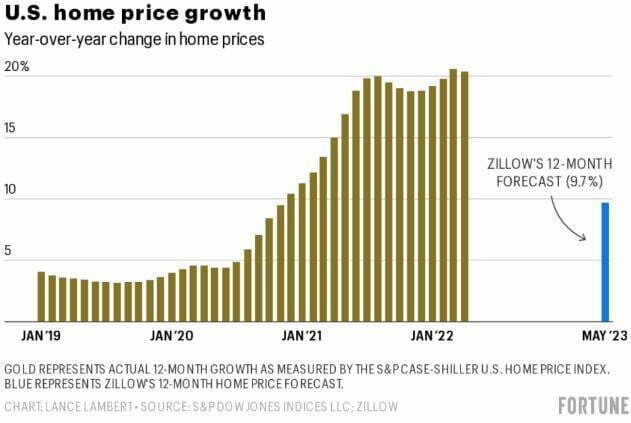

Wachter paints a pessimistic picture. “The housing market for sure is doomed; it’s a sinking ship.” The Zillow data graphed below also predicts a 9.7% decline in home price growth by early summer 2023.

If we step back from individual homeownership and look at the investment sector as a whole, including builders, building products companies, and home improvement players, the housing sector declined some 28% in 2022, underperforming the S&P 500, which declined by 20% over the same period. Interest rates are the primary driver.

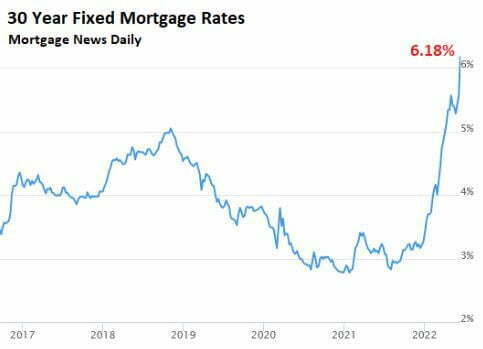

The average rate on 30-year fixed mortgages stands at about 6.4% currently, up from levels of just about 3.1% at the beginning of 2022, making financing home purchases more expensive. In addition, you have the median price of a home in the U.S. rose 10% last year, making it all the more unaffordable.

Housing starts for single-family homes fell to their lowest level since May of 2020.

The statistics bare out the macroeconomic environment and are changing the demographics of the landscape. An ever-increasing number of younger Americans are deciding to stay at home with their parents. This, coupled with the fact that family formation overall is in decline, is causing housing demand to dampen.

At the crux of this demand reduction is the underlying fear of recession and the possibility of job loss in the coming year. That’s little comfort to those in the real estate sector who are currently living through a recession. Wachter from Wharton says, “The housing market across the board is in a doom situation for a bit, but we are not about to see a recurrence of the systemic crisis that we had in 2012.”

That scenario is pretty much well echoed across the board of economists and real estate sector analysts.

The real estate recession is not just on the demand side. The supply of housing is another issue that continues to persist. We see a lack of supply on two fronts. One, single-family housing construction is down, but that’s short-term. Long term, we have a structural deficit in the housing supply. The reason home prices plummeted some 30% in the 2007-2012 downturn was that there was also an oversupply of properties. That is not the case currently, so one can expect that any doomsday scenario in 2023 shouldn’t be as bad as the last downturn.

This time around, it’s all about interest rates and mortgages. As long as the Fed keeps tightening and mortgage rates remain high, the real estate market will be in the tank.

As interest rates go up, and as mortgage rates go up, owners of homes with a 3% to 4% mortgage rate are not giving that up. They’re holding on to their homes and are not moving.

As we can see, the Fed is using the housing market to slow the overall economy down and to get the rate of inflation back to the target of 2%.

Let’s take a quick look at the rental market. It doesn’t take a genius to determine that if you can’t afford to buy in this market and don’t want to live in your parent’s basement, then renting is your option. Luckily, there has been a ton of construction in the multifamily housing market. So we currently have an oversupply of housing in this rental market, which should naturally lower rental prices from the demand side highs of 2021 and 2022.

Taking a big picture look at the possible real estate market next year, most pros are in consensus that it will be something of a transitional year characterized by uncertainty.

Markets hate uncertainty, and markets are ultimately people. According to Greg McBride, a chief financial analyst for Bankrate, “The housing market will be tepid in 2023, with only lukewarm demand and a limited amount of inventory available for sale. However, mortgage rates could pull back meaningfully next year if inflation pressures ease.”

If we see a year where rates don’t really move too much, you will continue to see fewer mortgages taken out as well as far less refinancing activity. Homeowners then may likely stay put, causing an uptick in home equity loans and lines of credit.