The housing industry has felt the wrath of inflation and interest rate increases more than other sectors in the financial markets.

As the year comes to a close, the red-hot housing market has been brought to its knees by soaring mortgage interest rates. The industry is quite cyclical as we know, and ebbs and flows with long-term government yields.

We are all aware of the Fed’s tightening stance, with recent rhetoric by Fed commissioners that they don’t have a total grip on inflation currently and forecast rates to remain high for the foreseeable future.

Rate increases have propelled mortgage rates to more than double their levels from a year ago, which has sapped buyer demand and begun to push home prices down from their peaks earlier this year.

The case against the housing market is quite clear.

There is a standoff between buyers and sellers coming off of one of the hottest sellers’ markets in decades.

On the buy side, home prices have begun to fall from their recent peaks, but not enough to make up for the rise in mortgage rates. This has basically priced most buyers out of the market.

On the sell side, sellers, who also become buyers upon the sale of their current residence, don’t want to give up their low rate mortgages to purchase new property at much higher rates.

According to economist Yelena Maleyev of KPMG US, “No one wants to catch a falling knife. No one wants to buy in a market when prices are falling. You want to wait it out.” This is the mindset of the retail real estate market. As such, the market is in a kind of status quo limbo.

Housing prices need to fall big time to make up for the meteoric rise in rates. In the past year, mortgage rates have risen from just under 3% to more than 7% for 30-year fixed-rate loans, according to Freddie Mac. So the question remains as to how low housing prices can go and what price point will lure buyers back into the market place.

Mark Zandi, chief economist at Moody’s Analytics expects prices will fall nationally by about 10% from peak to trough, bottoming out in the summer of next year. Even if prices drop in excess of 10%, we are coming off an historic run-up in prices post-pandemic.

Nationally, home list prices rose 40.6% in just over two years’ time, from March 2020, when the pandemic lockdowns began, to the peak of the market this past June, according to Realtor.com data. So a 10%, 15%, or even 20% drop over a two-year span isn’t as significant as it might seem at first.

However, on the real estate investment side, not everyone is anticipating a dramatic fall in prices, and toes are being put back into the pool of the real estate sector. Investors are taking a more sanguine approach, believing that inflation has peaked, and with it mortgage rates.

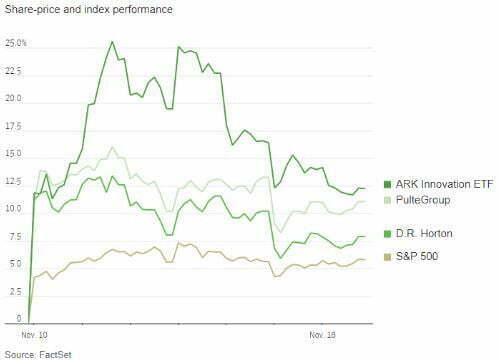

All you have to do is look at the recent moves in housing related stocks to see the trend change. Shares of real estate brokerages, home builders, mortgage lenders and practically anything that touches the housing industry have surged as well, outpacing the S&P 500’s 5.8% rise.

Recent CPI data suggests that the Fed may in fact begin to slowly reduce interest rates. Retail investors know this too, but those buying equities have the luxury of time on their side, as opposed to actual buyers who can’t take a risk on catching a falling knife with current market rates as high as they are.

Barometers like the PulteGroup and D.R. Horton are shown in the following chart to out pace the S&P 500.

Investors will closely watch upcoming economic releases on new home sales and consumer sentiment to gauge the health of the sector. Analysts must also account for the probability that this Fed-induced rate rise will push the economy further into recession.

Most, however, believe that we are not in an environment that resembles the financial crisis of 2008. Mortgage lenders have tightened underwriting standards and home builders haven’t taken on as much debt. Two indicators were ringing alarm bells in 2008.

Like you’re currently witnessing in the Big Tech sector, real estate firms are cutting costs and staff in an effort to shore up the balance sheet moving forward, preparing for the worst-case recession scenario. Redfin said on Nov. 9 that it was cutting 13% of its staff and shutting its home-flipping business to position itself to make money even if the housing market doesn’t recover for a while.

Just like the market itself, the time value of money over the long term is usually a solid approach to investment.

Unlike flipping properties or trading equities in the short term, buying this cyclical dip in the real estate sector will likely pay dividends in the long term. Bill Smead, chief investment officer at Smead Capital Management, said he has added in recent months to positions in D.R. Horton and Lennar.

Mr. Smead expects shares of home builders to perform strongly over the long run as the millennial generation settles down and buys homes.

If your time horizon is perhaps a decade or longer, then it’s likely that buying and holding the home builders now will result in healthy profits in the future.