As counter-intuitive as it may sound, increased borrowing from both the business and consumer sectors may mean that the economy is doing better than expected, and a draconian style recession may be avoided. What it does signal is that interest rates may perhaps have peaked with rate-reductions on the horizon. This bodes well for the overall health of the macro economy. Businesses and consumers alike are more prone to use financial leverage when they anticipate that cash flow will stay the same or increase, making it easier to bear the cost of borrowing.

Remember that consumer spending accounts for roughly two-thirds of overall GDP, and this spending was a key driver behind strong third quarter economic growth, with a surprisingly robust third quarter GDP coming in at an annualized rate of 4.9%. This is somewhat of a herculean task, in the midst of record inflationary rates and rising household debt. It’s possible that rising wages have helped propel this increase in consumer spending. As one might imagine, a large portion of that spending requires financing, such as home and auto purchases, as well as higher educational expenses.

Consumer spending and borrowing is a bellwether indicator for many analysts, giving them insight into which direction the economy may be headed. While it’s true that consumer debt is reaching record highs, real wages appear to be balancing things out, so not as to be a discernable problem. In Q2 of 2023, total household debt in the U.S. was $17.29 trillion, a roughly 5% increase over the debt held the year before. However, according to Rob Haworth, senior investment strategy director at U.S. Bank, “Debt level growth in recent months appears to be in line with wage growth, so at this point, it doesn’t seem to be raising a red flag.”

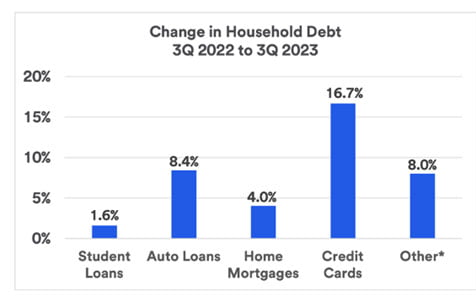

You can see from the chart above that the primary debt driver to the consumer currently is credit card debt, topping $1 trillion for the first time ever. This is in stark contrast to the decline in actual consumer debt that took place pursuant to the Covid pandemic. Now we’re finding an environment where inflation has been high, causing prices to rise, in conjunction with pandemic subsidies ending. This is the perfect storm to create consumer borrowing. The question is whether this is healthy or not. According to Matt Schoeppner, senior economist at U.S. Bank, “Consumers today appear to be protecting their balance sheets. They aren’t on a borrowing spree, but borrowing up to a point where it makes sense for them.”

The consumer side of the equation poses questions for the Fed in their interest policy going forward in 2024. Consumer spending at current levels will complicate matters in determining whether and how much to reduce interest rates. What the Fed is attempting to do is find the right rate that allows consumers to pull back spending to achieve their 2% inflation target.

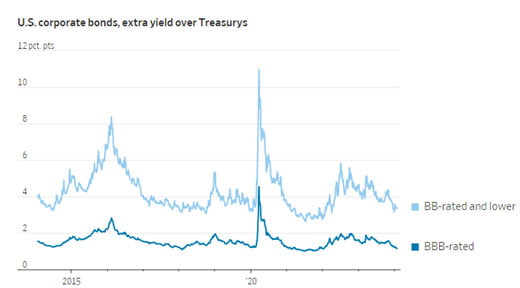

Let’s take a look at what’s happening on the business leveraging side. In anticipation of a Fed rate cut, the markets have driven the yield down on Treasuries, with investors now demanding less in additional yield for corporate debt instead of ultra-safe Treasurys.

Falling rates have helped spur a boom in the issuance of investment-grade corporate bonds, which is running at a near-record pace so far this year. The same holds true, though to a lesser extent, in the high yield bond market. Riskier companies are issuing debt at levels much greater than in 2022, when rates were rising, and no upside end was in sight. In the M&A market, new deals have also increased, including loans used to pay dividends to shareholders.

It wasn’t too long ago when the market had serious concerns over the stability of the banking system, in particular the small and medium sized banks, in light of the failure of Silicon Valley Bank et al. Recently though, data have shown a decline in the share of banks that are tightening their lending standards. This is good news for business, since the last several years of inflation have affected their balance sheets, in particular making inventory that much more expensive to buy and hold.

No one has a crystal ball into the future, but statistics on the borrowing of businesses and consumers can help point one in the right direction. The tide appears to be turning in the direction of a stronger economy as such, flying in the face of many financial pundits. If borrowing data is strong currently, the anticipation of future Fed rate cuts will only add fuel to the fire. While anything can happen in an election year, it seems plausible that politically speaking we will maintain the status quo, or perhaps see better economic data. Neither party wants to campaign on a dire economy.