As the saying from the iconic movie Jaws goes, “So you thought it was safe to go back in the water,” so goes the mantra that you thought your local or regional bank might be safe as well.

After the collapse of First Republic and the others, you might have thought that it would be okay to dip your toes back in the water, but as JPMorgan Chase CEO Jamie Dimon delivered, “This part of the crisis is over,” suggesting more pain on the back end in the future.

A perfect banking storm of rising interest rates, losses on commercial real estate, and heightened regulatory scrutiny suggest a wave of banking consolidation not seen since the savings and loan crises of 2008.

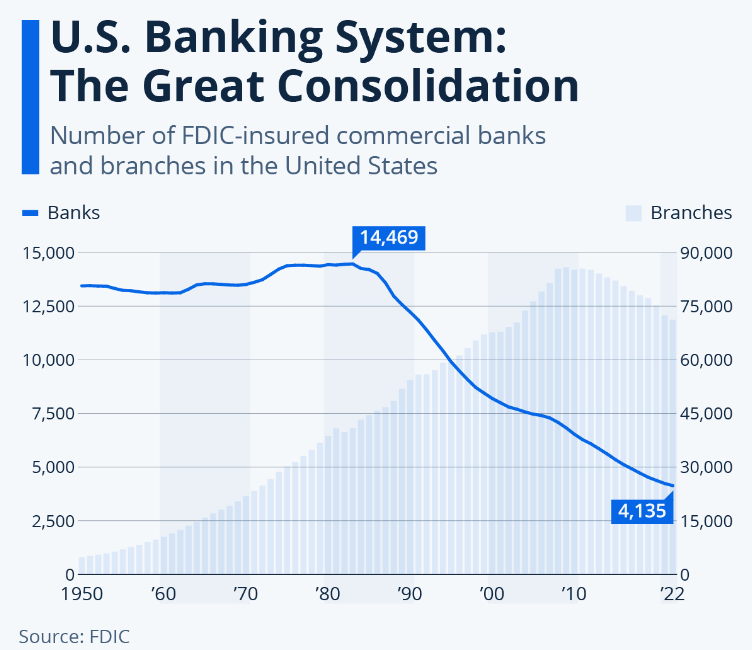

Simply stated, the U.S. has more federally insured banking institutions than any country in the world. To continue with the nautical analogies, like fish, regional banks will either eat, or be eaten.

So how did we get into this mess? Pursuant to the banking crisis of 2008, regulators ironically brought more scrutiny and regulation to the supposed larger banks that were too big to fail, which were those with assets of $250 billion or more. Oversight in the way of stress tests as well as balance sheet measures were put in place that would provide a cushion against unforeseen losses.

All of this has worked well for the larger institutions, but as you have guessed, the smaller banks have gotten lost in the regulatory forest.

Banks make money by using your money. You have been lulled to sleep over the last decade with your time and demand deposits returning you practically nothing. Low cost funding in the form of bonds made banking easy and profitable during this period. Things have changed. Interest rates have risen and are predicted to travel higher.

Cheap financing in the form of bonds has dried up. Customers have awaken and are fleeing regional banks in droves for the lure of higher interest rates on their savings in online banks like Capital One and others. According to Brian Graham, a banking veteran and co-founder of advisory firm Klaros Group, “For at least 15 years, banks have been awash in deposits and with low rates, it cost them nothing.”

Again, banks can’t make money without your money or cheap money.

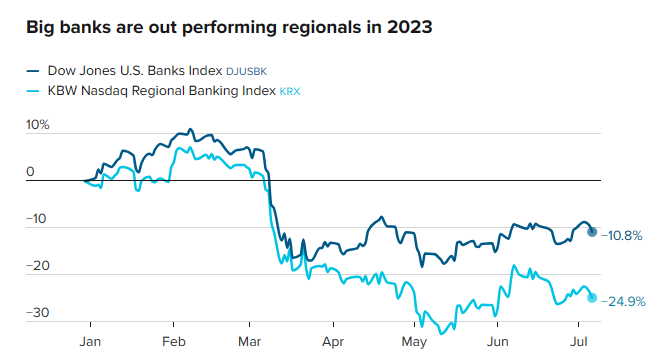

If you don’t believe me, just take a look at the equity markets. While in negative territory year to date, big banks outperform their smaller brethren by more than two to one.

In typical authoritarian progressive style, let no good crisis go without the opportunity to take more control of the free market. According to Chris Wolfe, a Fitch banking analyst who previously worked at the Federal Reserve Bank of New York, “There’s going to be a lot more costs coming down the pipe that’s going to depress returns and pressure earnings.

Higher fixed costs require greater scale, whether you’re in steel manufacturing or banking.”

Banks that have lost a significant portion of their deposit base, perhaps 10% to 20% will be in for trouble. These banks have basically two options, to raise capital at a higher cost or sell themselves to larger institutions.

A third option depending upon the duration of the bond portfolio that they currently hold would be to ride out the storm and let these bonds mature at par and roll off the balance sheet.

The next shoe to drop will likely be the release of second quarter bank earnings. It’s somewhat of a foregone conclusion that the stated macroeconomic environment will bring about lower earnings.

This will bring about another loop of negative feedback.

Lower earnings will suppress stock prices, which will lead to deposit flight. Banks are looking at basically everything on their balance sheets, trying to determine what they can sell at reasonable prices that could help shore things up.

When all else fails, outright consolidation is next.

Regulators actually encourage this in tumultuous times. According to Ken Tumin, senior industry analyst at LendingTree, “It’s very common for the FDIC to arrange for large banks to acquire failed banks.”

So, in other words, the big banks may just keep getting bigger.

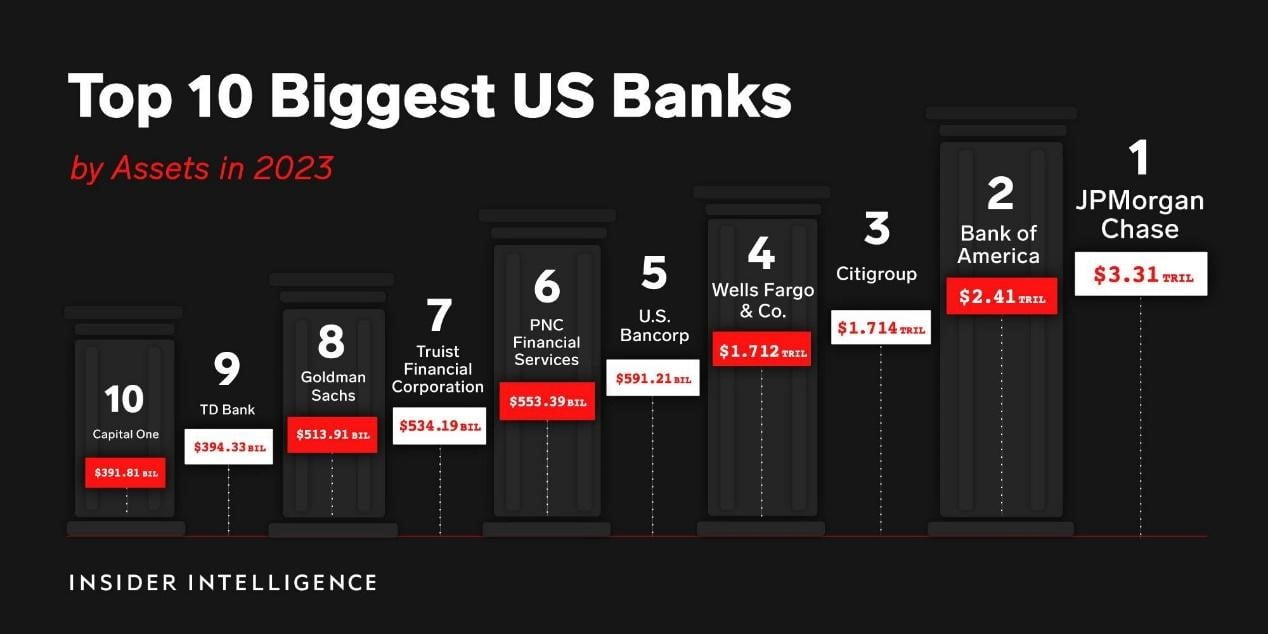

If you’re wondering whether your bank is one of the big boys, the following chart shows the top ten.

So what exactly does merger mania in the banking industry mean for you? As a depositor, make sure you keep deposits under FDIC coverage limits at your bank.

As an investor you have to remember that if regulators decide to shut down a bank the stock price can get wiped out completely. Hence the downward spiral of the regional bank stock index this year.

Buckle up for a turbulent ride for the remainder of the year.